Wednesday, July 30, 2014

Pending Home Sales Slip in June

After three consecutive months of solid gains, pending home sales slowed modestly in June, according to theNational Association of Realtors®.

The Pending Home Sales Index,* a forward-looking indicator based on contract signings, declined 1.1 percent to 102.7 in June from 103.8 in May, and is 7.3 percent below June 2013 (110.8). Despite June’s decrease, the index is above 100 – considered an average level of contract activity – for the second consecutive month after failing to reach the mark since November 2013 (100.7).

Lawrence Yun, NAR chief economist, says the housing market is stabilizing, but ongoing challenges are impeding full sales potential. “Activity is notably higher than earlier this year as prices have moderated and inventory levels have improved,” he said. “However, supply shortages still exist in parts of the country, wages are flat, and tight credit conditions are deterring a higher number of potential buyers from fully taking advantage of lower interest rates.”

Despite these headwinds, Yun ultimately expects a slight uptick in sales during the second half of the year. “The good news is that price appreciation has decreased to its slowest pace since March 20121 behind much needed increases in inventory,” he said. “With rents rising 4 percent annually, potential buyers are less likely to experience sticker shock and can make smart decisions on whether or not it makes sense to buy or continue renting.”

The PTC Index for June

With the summer in full swing, the PTC Index inched just slightly to settle at 221 points for the month of June. Overall, most categories showed little change from the month prior and, in some cases, little from the year-ago time period. First, building permits and existing home sales fell from the month prior by 8.4 percent and 4.2 percent, respectively. Refinances also slipped slightly from the month prior, but show some stabilization month-over-month having fallen by only 4/5 of a point. Notices of default also stabilized with no change from the month prior but down by 45 percent from a year ago. Inventories of distressed property (short sales/REOs) dipped by 3.9 percent, while new home sales saw a boost in June with a 20.5 percent increase from the month prior and almost equal to numbers from this time last year. Finally, the average Treasure Valley sales price inched up just a bit to settle at $201,539 - a 5 percent increase from June 2013.

June 2014

Building Permits

261

New Home Sales

206

Existing Home Sales

902

Refinance

724

Average Sales Price

201539.5

Financial-Bond Market(10-yr Treasury)

2.6

Days on Market

53

Distressed(Short Sales and REO)

956

Notices of Default

112

PTC Index

221

From Pioneer Title Company

To create the PTC Index, we gather data for nine key real estate variables and process them through our weighted algorithm to generate a single number reflective of the Treasure Valley real estate market.

The base data for the PTC Index is culled from various private sources as well as the public domain on a monthly basis.

These nine variables include building permits, new home sales, existing home sales refinances, average home sales price, the 10-year Treasury yield, days on market, distressed (short sales and Real Estate Owned) and notices of default. In simplified terms, the negative data from these sources is subtracted from the positive data to create the PTC Index. But before this happens, the data is weighted using a proprietary computation, resulting in a more accurate reflection of the real estate market.

Friday, July 25, 2014

What is holding back the Real Estate Market?

Though the housing market is recovering nicely, it is not doing quite as well as some analysts had predicted. There has been no shortage of excuses offered as to why this is: the rise in interest rates, more stringent lending standards, the weather.

However, we feel that there is one factor that is most responsible for curtailing the number of houses sold – the number of houses available for sale!

Inventory Levels are BELOW Historic Norms

In a recent economic forecast, Freddie Mac addressed this exact issue:

“Including newly built homes in the inventory count, the total number of homes offered for sale relative to the number of households in the U.S. has been running at the lowest level in more than 30 years, as shown in the second exhibit. The relatively low for-sale inventory reflects several features of today’s market.”

“A supply-constrained market (holding other factors constant) will result in a decline in the volume of sales and an increase in real transaction prices.”

NAR Report Confirms Inventory Constriction

History shows us that a balanced real estate market requires a six month supply of available housing inventory. The National Association of Realtors released their Existing Homes Sales Report earlier this week. The report revealed that we are still only at a 5.5 month supply of homes for sale. We have not reached the 6 month mark in over two years.

The recent increase in buyers now looking will again put a strain on this number. That is why today at 2PM EST, we are hosting a special webinar for real estate professionals; The 4 Keys to Prospecting for Listings that Sell. Agents can reserve their seat here.

Bottom Line

While inventory levels remain below historic norms, it will remain a seller’s market. This being the case, if you are considering selling your home, now may be the time to list it for sale.

Thursday, July 24, 2014

Foreclosure Inventory Down 37% over Last Year!

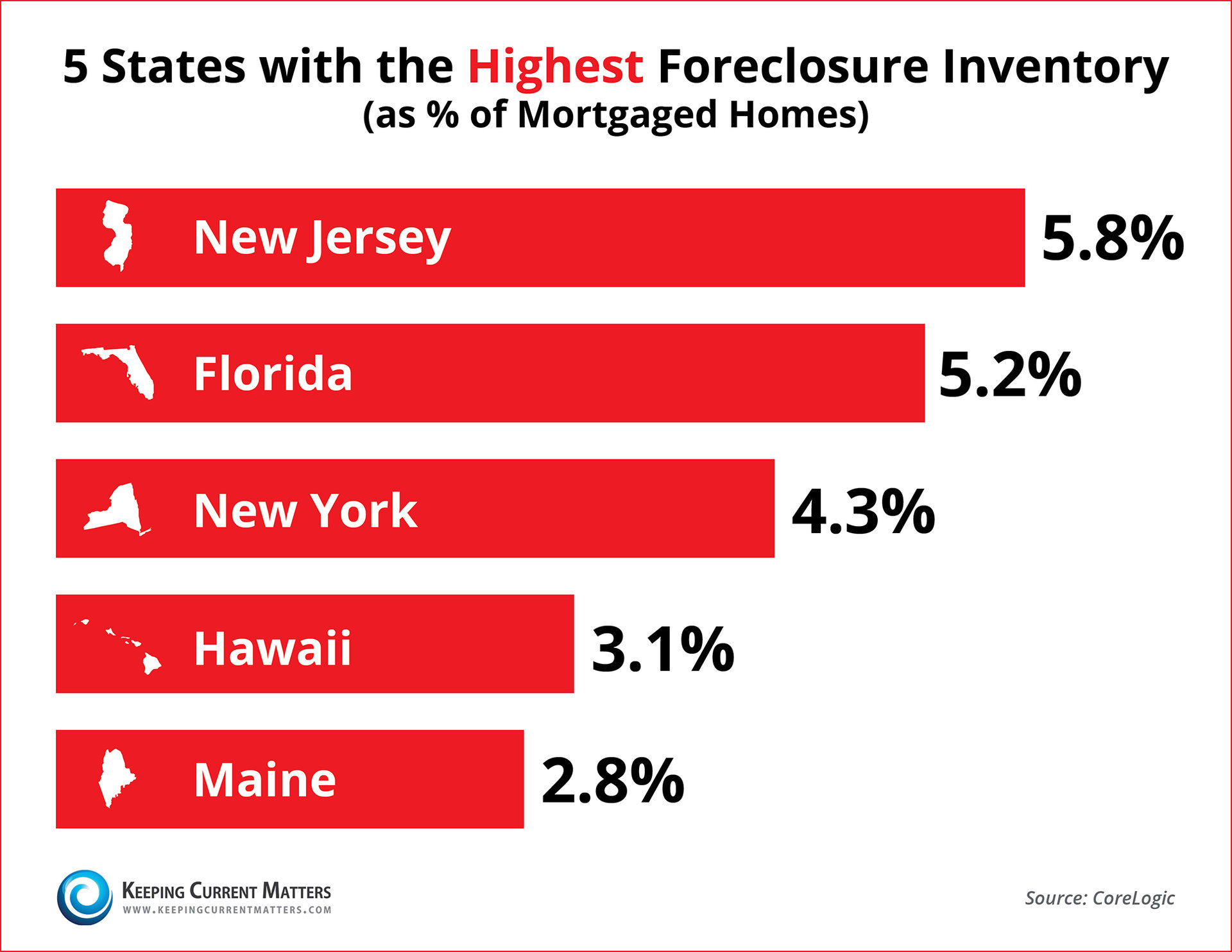

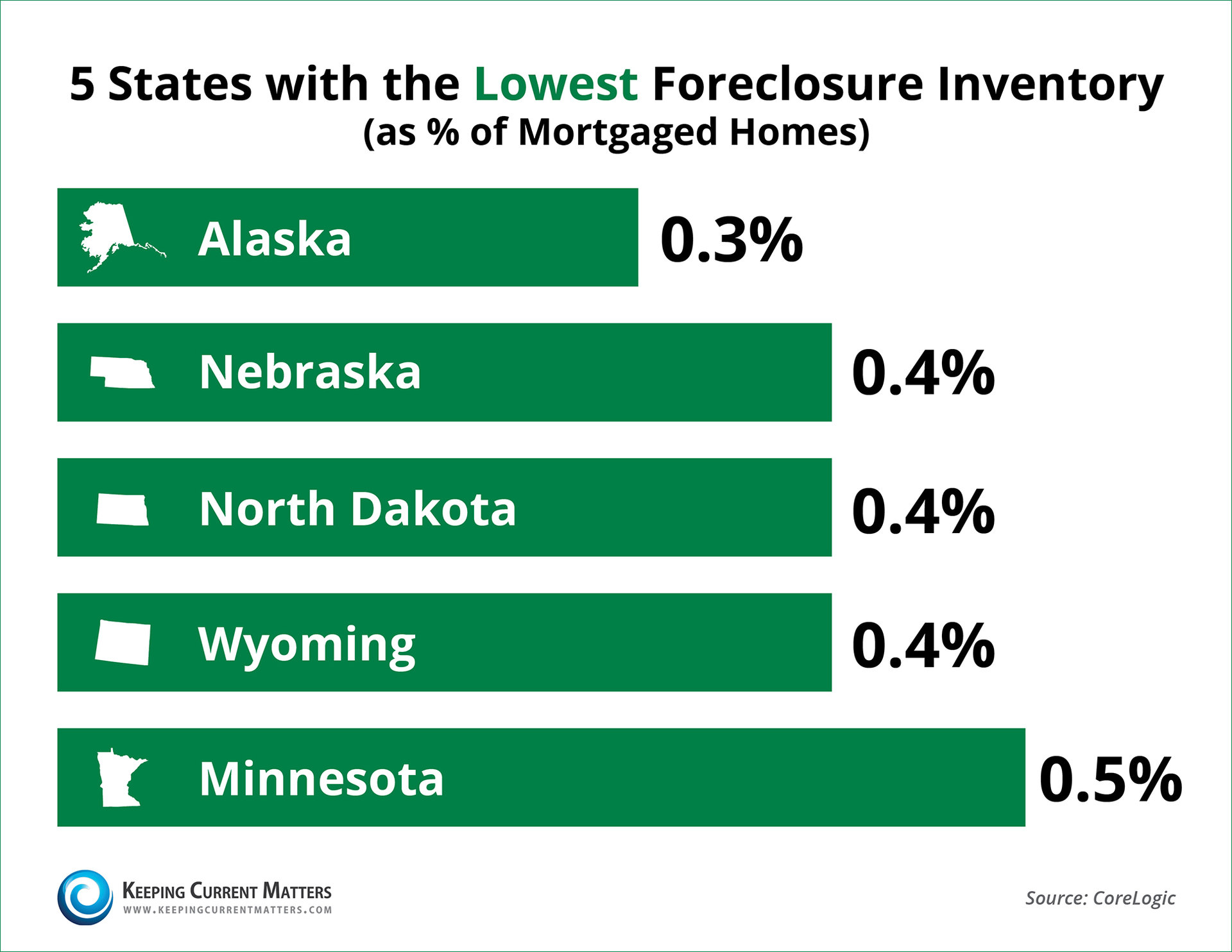

According to the latest CoreLogic National Foreclosure Report, “approximately 660,000 homes in the US were in some state of foreclosure as of May 2014”. This figure is down 37% from the 1 million homes in May of 2013. May marked the 31st consecutive month in which there were year-over-year declines. Mark Fleming chief economist for CoreLogic revealed: “Significant gains have been made in the last year to reduce the foreclosure stock. Yet, these improvements are occurring disproportionately in non-judicial states. The foreclosure inventory in judicial states is averaging 2.1% which is more than twice the 0.9% average that is occurring in non-judicial states.” The foreclosure process in the twenty-two judicial states can take, on average, anywhere from 180-400 days according to the Mortgage Bankers Association. The lack of initial court intervention in non-judicial states, often means that the process of foreclosure takes significantly less time. Therefore, judicial states as a whole, have taken longer to catch up to the rest of the country in liquidating foreclosure inventory. All five states with the highest foreclosure inventory as a percentage of mortgaged homes are judicial states.  On the list of the five lowest inventory states, only North Dakota uses a judicial process.  Bottom LineEven though some states have not recovered completely from the foreclosure crisis, the nation as a whole is on the right track as inventory decreases. |

Monday, July 14, 2014

Sunday, July 13, 2014

June Market Report for Ada County – Longer Busier Days

by Marc Lebowitz, RCE, CAE

ACAR Executive Director

Single family home sales in June 2014 were 798 in Ada County, a decrease of 3% compared to June 2013. YTD total sales are down 2% compared to this time last year; 3,682 homes sold compared to 3,776.

In June 76% of our total sales were for homes priced above $160,000.

In June sales of homes in the $300,000 – $400,000 were up 25% from May 2014 to 140. This category had the greatest sales increase month-over-month and was the third highest sales category behind $120,000 - $160,000 and $160,000 - $200,000.

Days on Market for June were 46; one day less than last month. In June 2013, Days on Market was 46.

New homes sold in June totaled 151; down 10% from last year; but…up 13% over May.

Existing home sales were 647; down 2% from June 2013.

Historically, comparing June sales to May is sort of a mixed bag. Two times between 2001 and 2014 June sales were ahead of May sales by double digits. Six times the increase was marginal. Three times sales went down. June 2014 posted a 2% increase over May.

Pending sales at the end of June were 1126; down 18% from June 2013. Pending sales have trailed behind previous year’s pending sales for eleven consecutive months.

June median home price was $218,650; up 4% from June 2013. Our YTD median price is $207,500; up 8% over last year.

New Homes median price for June was $325,900; up 22% from June 2013. For Existing homes the increase is 2% to $199,900.

The number of houses available for sale at the end of June increased 4% from May 2014 to 2,789. This is an increase we really need…maybe. This is 32% more than last year at this time.

We anticipate continued inventory growth from now until the end of Summer.

The price point with the largest increase month-over-month is $250,000 – $300,000 at 11%. The next highest is $200,000 – $250,000 with 10%. Below $160,000 there is no increase in availability.

In Ada County we now have 3.5 months of inventory on hand, down 5% from the end of May.

The price categories in shortest supply are $100,000 - $120,000 and $120,000 to $160,000 which both have 1.8 months; actually up a little from last month.

From $160,000 to $400,000 we have 3.6 months; not much change from last month.

Of sales in June, the most popular price point was $160,000 to $200,000 (21%); and $120,000 to $160,000 (20%) followed by $300,000 to $400,000 with 17%.

So…what’s next?

I predicted June’s sales would be ahead of June 2013. I missed it by 28 sales. When you look at the sales trend graph you can see how close we are to last year’s booming Summer. Looking a the same chart you can see that last July was huge. Are we going to repeat that. I don’t think so. I am still convinced that the third quarter wikk be our recovery quarter and put us back ahead of last year.

I was right on the median price prediction; but I think that will slide back closer to $205,000 in July.

NPR reported yesterday that the Fed was going to exit “quantitative easing” in October. This will, almost certainly, increase mortgage rates as we go into the fourth quarter.

We also saw last week that unemployment numbers are down to 6%.

All in all, I’m still feeling pretty good about how we will finish he year.

Boise found its way on to a few more “Best Of” lists” in June. We scored on “Biking and Beer”, “Family Friendly”, “Best Looking Men” and “Best Secret Ski Towns” (McCall actually, but close enough) and dodged “Most Expensive” and “Most Stressful”.

We also read that the Greenbelt was the place in town to find the smartest happiest Boiseans. Tell me something I don’t know.

ACAR Executive Director

Single family home sales in June 2014 were 798 in Ada County, a decrease of 3% compared to June 2013. YTD total sales are down 2% compared to this time last year; 3,682 homes sold compared to 3,776.

In June 76% of our total sales were for homes priced above $160,000.

In June sales of homes in the $300,000 – $400,000 were up 25% from May 2014 to 140. This category had the greatest sales increase month-over-month and was the third highest sales category behind $120,000 - $160,000 and $160,000 - $200,000.

Days on Market for June were 46; one day less than last month. In June 2013, Days on Market was 46.

New homes sold in June totaled 151; down 10% from last year; but…up 13% over May.

Existing home sales were 647; down 2% from June 2013.

Historically, comparing June sales to May is sort of a mixed bag. Two times between 2001 and 2014 June sales were ahead of May sales by double digits. Six times the increase was marginal. Three times sales went down. June 2014 posted a 2% increase over May.

Pending sales at the end of June were 1126; down 18% from June 2013. Pending sales have trailed behind previous year’s pending sales for eleven consecutive months.

June median home price was $218,650; up 4% from June 2013. Our YTD median price is $207,500; up 8% over last year.

New Homes median price for June was $325,900; up 22% from June 2013. For Existing homes the increase is 2% to $199,900.

The number of houses available for sale at the end of June increased 4% from May 2014 to 2,789. This is an increase we really need…maybe. This is 32% more than last year at this time.

We anticipate continued inventory growth from now until the end of Summer.

The price point with the largest increase month-over-month is $250,000 – $300,000 at 11%. The next highest is $200,000 – $250,000 with 10%. Below $160,000 there is no increase in availability.

In Ada County we now have 3.5 months of inventory on hand, down 5% from the end of May.

The price categories in shortest supply are $100,000 - $120,000 and $120,000 to $160,000 which both have 1.8 months; actually up a little from last month.

From $160,000 to $400,000 we have 3.6 months; not much change from last month.

Of sales in June, the most popular price point was $160,000 to $200,000 (21%); and $120,000 to $160,000 (20%) followed by $300,000 to $400,000 with 17%.

So…what’s next?

I predicted June’s sales would be ahead of June 2013. I missed it by 28 sales. When you look at the sales trend graph you can see how close we are to last year’s booming Summer. Looking a the same chart you can see that last July was huge. Are we going to repeat that. I don’t think so. I am still convinced that the third quarter wikk be our recovery quarter and put us back ahead of last year.

I was right on the median price prediction; but I think that will slide back closer to $205,000 in July.

NPR reported yesterday that the Fed was going to exit “quantitative easing” in October. This will, almost certainly, increase mortgage rates as we go into the fourth quarter.

We also saw last week that unemployment numbers are down to 6%.

All in all, I’m still feeling pretty good about how we will finish he year.

Boise found its way on to a few more “Best Of” lists” in June. We scored on “Biking and Beer”, “Family Friendly”, “Best Looking Men” and “Best Secret Ski Towns” (McCall actually, but close enough) and dodged “Most Expensive” and “Most Stressful”.

We also read that the Greenbelt was the place in town to find the smartest happiest Boiseans. Tell me something I don’t know.

Is Residential Real Estate Really a ‘Crapshoot’?

From KCM Blog

Our founder, Steve Harney, occasionally asks to do a personal post on what he sees as important to our industry. Today is one of those days. Enjoy! – The KCM Crew That is what a headline announced in a CNNMoney post Monday. They were quoting Karl Case “an economist whose name is synonymous with home prices. He is co-creator of the much watched S&P/Case-Shiller home price indexes with Bob Shiller, who won the Nobel Prize in economics last year.” Case did explain that the commonly held belief that housing prices could ‘never’ depreciate was corrected over the last decade. And it is true that Case referenced a home he bought during that time had lost almost half its value. However, there were other comments attributed to Case in the article:

He bet on three houses; one lost 50%, one gained over 400% and the other gained approximately 300%. Sounds like great odds to me. Give me the dice and get out of my way.Last week, John Maxfield, in a The Motley Fool blog post, wrote: “Over the past year, [home prices] are up by 8.9%. Over the past two years, they're up by 19.7%. Over the past three years, they're up by 23%. And there's little evidence that this trend is coming to an end anytime soon… [It] should be obvious why now is such an opportunistic time to buy a house. Of course, if you want to wait, that's up to you. But doing so could very well be a source of regret later on down the road.” Give me the dice and get out of my way.If buying residential real estate is actually a crapshoot (as the headline claimed), it seems the odds are in the shooter’s hand. PLEASE give me the dice and get out of my way. I really want to roll. |

Saturday, July 12, 2014

National Association of Realtors: Two Reasons to Sell Now

We all realize that the best time to sell anything is when demand is high and the supply of that item is limited. The last two major reports issued by the National Association of Realtors (NAR) revealed information that suggests that now may be the best time to sell your house. Let’s look at the data covered by the latest Pending Home Sales Report and Existing Home Sales Report.

THE PENDING HOME SALES REPORT

The report announced that pending home sales (homes going into contract) “surged” by 6.1%. The increase was “the largest month-over-month gain since April 2010, when first-time home buyers rushed to sign purchase contracts before a popular tax credit program ended”. Lawrence Yun, NAR’s chief economist, expects improving home sales throughout the rest of the year: “Sales should exceed an annual pace of five million homes in some of the upcoming months behind favorable mortgage rates, more inventory and improved job creation.” Takeaway: Demand is beginning to increase dramatically compared to earlier in the year.

THE EXISTING HOME SALES REPORT

The most important data point revealed in the report was not sales but instead the inventory of homes on the market (supply). The report explained:

- Total housing inventory climbed 2.2% to 2.28 million homes available for sale

- That represents a 5.6-month supply at the current sales pace

- Unsold inventory is 6.0% higher than a year ago

There were two more interesting comments made by Yun in the report:

- “Rising inventory bodes well for slower price growth and greater affordability, but the amount of homes for sale is still modestly below a balanced market.” In real estate, there is a guideline that often applies. When there is less than 6 months inventory available, we are in a sellers’ market and we will see appreciation. Between 6-7 months is a neutral market where prices will increase at the rate of inflation. More than 7 months inventory means we are in a buyers’ market and should expect depreciation in home values. As Yun notes, we are currently in a sellers’ market (prices still increasing) but are headed to a neutral market.

- "New home construction is still needed to keep prices and housing supply healthy in the long run.” As new construction begins to be built, there will be increased downward pressure on the prices of existing homes on the market.

Takeaway: Supply is about to increase significantly. The supply of existing homes is already increasing and the number of newly constructed homes is about to increase.

Bottom Line

If you are going to sell, now may be the time.

Friday, July 11, 2014

Treasure Valley's Vanishing Apartment Vacancies.

From the Idaho Statesman

A look at Treasure Valley rent statistics.

As it has become harder for individuals and families to find rentals in the Treasure Valley, prices have risen almost across the board. Vacancy rates were 2.2 percent lower in the first quarter of the year than in the fourth quarter of 2013.

The decrease was more extreme for year-over-year vacancy rates, which fell from 2.6 percent in the first quarter of 2013 to 1.7 percent during the same three-month period this year.

The Southwest Idaho Chapter of the National Association of Residential Property Managers says demand for rentals is at a tipping point, close to overtaking the supply of available units. Most of the latest growth in rental prices has been in single-family homes, the chapter said in its quarterly analysis. Rental rates tend to be higher in spring than in winter even without a drop in vacancies.

See Treasure Valley rent statistics

A look at Treasure Valley rent statistics.

As it has become harder for individuals and families to find rentals in the Treasure Valley, prices have risen almost across the board. Vacancy rates were 2.2 percent lower in the first quarter of the year than in the fourth quarter of 2013.

The decrease was more extreme for year-over-year vacancy rates, which fell from 2.6 percent in the first quarter of 2013 to 1.7 percent during the same three-month period this year.

The Southwest Idaho Chapter of the National Association of Residential Property Managers says demand for rentals is at a tipping point, close to overtaking the supply of available units. Most of the latest growth in rental prices has been in single-family homes, the chapter said in its quarterly analysis. Rental rates tend to be higher in spring than in winter even without a drop in vacancies.

See Treasure Valley rent statistics

Thursday, July 10, 2014

Buying a Home Know Your Options!

In a post earlier this week, we suggested that the Millennial generation’s struggles with student debt and the overarching concept of homeownership are not the reasons for so many first time buyers hesitating to move forward with the purchase of their first home. Now there is another firm suggesting the same. The asset management company, Nomura, came out with strong guidance to their investors. According to an article in Housing Wire last week:

“Nomura’s note to clients has a take few have offered: The first time homebuyers are holding out and it’s not student debt, a shift away from homeownership as a choice by Millennials, or any of that.”

Instead, they think it is a lack of a full understanding of the mortgage process. The article explains:

“Analysts say it’s not that Millennials and other potential homebuyers aren’t qualified in terms of their credit scores or in how much they have saved for their down payment. It’s that they think they’re not qualified or they think that they don’t have a big enough down payment.”(emphasis added)

This comes off the heels of a survey by Zelman & Associates that revealed that 38% of those between the ages of 25-29 years old and 42% of those between the ages of 30-34 years old believe that a minimum of 15% is required as a down payment to purchase a home. In actually, a purchaser may be able to put down far less.

The Reality of the Situation

According to Christina Boyle, Freddie Mac’s VP and Head of Single-Family Sales & Relationship Management, in a recent Executive Perspectives piece:

- A person “can get a conforming, conventional mortgage with a down payment of as little as 5 percent (sometimes with as little as 3 percent coming out of their own pockets)”.

- Freddie Mac's purchase of mortgages with down payments under 10 percent more than quadrupled between 2009 and 2013.

- More than one in five borrowers who took out conforming, conventional mortgages in 2014 put down 10 percent or less.

- Qualified borrowers can further reduce the down payment coming out of their own pockets to 3 percent by lining up gifts from family or grants or loans from non-profits or public agencies.

Ms. Boyle goes on to explain:

“Letting more consumers know how down payments are determined could bring more qualified borrowers off the sidelines. Depending on their credit history and other factors, many borrowers can expect to make a down payment of about 5 or 10 percent.”

Bottom Line

If you have considered purchasing a house or moving-up to a new dream home, know all of your options. Reach out to a real estate and/or mortgage professional in your marketplace to get the best, most up-to-date information available. You may be surprised to learn what you and your family are capable of achieving.

Wednesday, July 9, 2014

Home Building Heats Up in the Treasure Valley

After the Treasure Valley housing market collapsed in 2008, new homes that previously sold like Girl Scout cookies sat empty with “For Sale” signs graying in their front yards.

Corey Barton, owner of Meridian’s CBH Homes and one of the most prolific builders in the Valley, came up with a plan to sell off some of his pent-up inventory. The “Deal of a Lifetime” was a clearance sale. CBH Homes closed deals on about 200 houses for as much as 70 percent below their listed prices.

Barton said the sale helped CBH Homes keep cash moving through what he thought would be the end of a slow period for builders. He didn’t know that the true low-water mark wouldn’t come until 2011. That year CBH Homes built about 300 homes, down nearly 82 percent from its 2005 peak of 1,650.

“Every year, we couldn’t believe the market kept going down and going down,” Barton said. “We kept building and purchasing all the way through the bottom.”

To the relief of Barton and many others, the market showed signs of life in 2012 and surged in 2013, bringing work to almost all types of home contractors and subcontractors, though some — such as certain niche contractors who specialize in work on existing, high-end homes — have been left behind. Barton said he sold 725 homes last year and is on pace to sell 950 this year. But that total still would be down about 40 percent from 2006.

Improved lending practices have cut down on his company’s potential market but also have removed the risk of another bubble, he said.

“We’re getting back to where property values, population and job growth are all in equilibrium,” Barton said. “I think back to normal would be in a few years.”

In 2012, 1,997 new residential structures were added to the property-tax roll in Ada County, according to the county assessor’s office. That number increased to 2,534 last year, still well below the county’s 2005 peak of 6,491.

The recession was devastating for the entire Valley home-building industry. Permits for residential improvements in Ada County — including new home permits — dropped from 6,491 in 2005 to 1,232 in 2011, a 73 percent decline, according to the Ada County Assessor’s Office.

CBH Homes cut its payroll from 100 employees to 50 during the slowdown. The number of licensed contractor entities and professionals in Idaho fell 25 percent from 2007 to 2012, according to the Idaho Bureau of Occupational Licenses.

In 2013, Barton said CBH Homes had a hard time finding employees and subcontractors to keep up with its increased building. Too many moved away or changed professions during the recession, he said. But Barton expects the workforce to come back with the increase in demand. He has 60 employees now.

“The workforce is getting a little stronger to where the availability of skilled labor is improving,” he said.

Jeff Thompson is president of both the Building Contractors Association of Southwestern Idaho and of Meridian’s Thompson Homes, which makes houses priced at $500,000 and up. He said all association members are busy. His company is on pace this year to return to the six to 14 houses per year it averaged before the downturn.

“Midway through 2012 was when the phone started ringing again,” Thompson said. “We’re already seeing an increase in inquiries this year. It’s solid. It’s a really good sign for us.”

Barton said homebuyers and mortgage lenders needed to watch home values rebound before they could shop and lend with confidence.

“Everybody’s active right now,” Barton said. “It’s kind of like a cut on your hand. It starts to heal, it slowly gets better, and then it’s back to normal.”

Pockets of the home-building industry haven’t recovered.

Boise contractor Guy Shinn, of Guy Shinn Painting, specializes in high-end painting on existing homes. His customers are typically wealthy or upper-middle class homeowners willing to pay for staining, window glazing and varnishing.

Shinn said he now bids 20 percent less than he did in 2007, and he has cut his employee roster from 19 to six. Now, Shinn said he’s about to go out of business. Other niche painting, taping and floor-covering contractors are also struggling, he said.

“Six months into the recession, I thought it would go on for a year,” he said. “It’s taken me six years to finally worry about it.”

Read more here: http://www.idahostatesman.com/2014/03/04/3060570/home-building-heats-up-in-valley.html#storylink=cpy

Corey Barton, owner of Meridian’s CBH Homes and one of the most prolific builders in the Valley, came up with a plan to sell off some of his pent-up inventory. The “Deal of a Lifetime” was a clearance sale. CBH Homes closed deals on about 200 houses for as much as 70 percent below their listed prices.

Barton said the sale helped CBH Homes keep cash moving through what he thought would be the end of a slow period for builders. He didn’t know that the true low-water mark wouldn’t come until 2011. That year CBH Homes built about 300 homes, down nearly 82 percent from its 2005 peak of 1,650.

“Every year, we couldn’t believe the market kept going down and going down,” Barton said. “We kept building and purchasing all the way through the bottom.”

To the relief of Barton and many others, the market showed signs of life in 2012 and surged in 2013, bringing work to almost all types of home contractors and subcontractors, though some — such as certain niche contractors who specialize in work on existing, high-end homes — have been left behind. Barton said he sold 725 homes last year and is on pace to sell 950 this year. But that total still would be down about 40 percent from 2006.

Improved lending practices have cut down on his company’s potential market but also have removed the risk of another bubble, he said.

“We’re getting back to where property values, population and job growth are all in equilibrium,” Barton said. “I think back to normal would be in a few years.”

In 2012, 1,997 new residential structures were added to the property-tax roll in Ada County, according to the county assessor’s office. That number increased to 2,534 last year, still well below the county’s 2005 peak of 6,491.

The recession was devastating for the entire Valley home-building industry. Permits for residential improvements in Ada County — including new home permits — dropped from 6,491 in 2005 to 1,232 in 2011, a 73 percent decline, according to the Ada County Assessor’s Office.

CBH Homes cut its payroll from 100 employees to 50 during the slowdown. The number of licensed contractor entities and professionals in Idaho fell 25 percent from 2007 to 2012, according to the Idaho Bureau of Occupational Licenses.

In 2013, Barton said CBH Homes had a hard time finding employees and subcontractors to keep up with its increased building. Too many moved away or changed professions during the recession, he said. But Barton expects the workforce to come back with the increase in demand. He has 60 employees now.

“The workforce is getting a little stronger to where the availability of skilled labor is improving,” he said.

Jeff Thompson is president of both the Building Contractors Association of Southwestern Idaho and of Meridian’s Thompson Homes, which makes houses priced at $500,000 and up. He said all association members are busy. His company is on pace this year to return to the six to 14 houses per year it averaged before the downturn.

“Midway through 2012 was when the phone started ringing again,” Thompson said. “We’re already seeing an increase in inquiries this year. It’s solid. It’s a really good sign for us.”

Barton said homebuyers and mortgage lenders needed to watch home values rebound before they could shop and lend with confidence.

“Everybody’s active right now,” Barton said. “It’s kind of like a cut on your hand. It starts to heal, it slowly gets better, and then it’s back to normal.”

Pockets of the home-building industry haven’t recovered.

Boise contractor Guy Shinn, of Guy Shinn Painting, specializes in high-end painting on existing homes. His customers are typically wealthy or upper-middle class homeowners willing to pay for staining, window glazing and varnishing.

Shinn said he now bids 20 percent less than he did in 2007, and he has cut his employee roster from 19 to six. Now, Shinn said he’s about to go out of business. Other niche painting, taping and floor-covering contractors are also struggling, he said.

“Six months into the recession, I thought it would go on for a year,” he said. “It’s taken me six years to finally worry about it.”

Read more here: http://www.idahostatesman.com/2014/03/04/3060570/home-building-heats-up-in-valley.html#storylink=cpy

Subscribe to:

Posts (Atom)