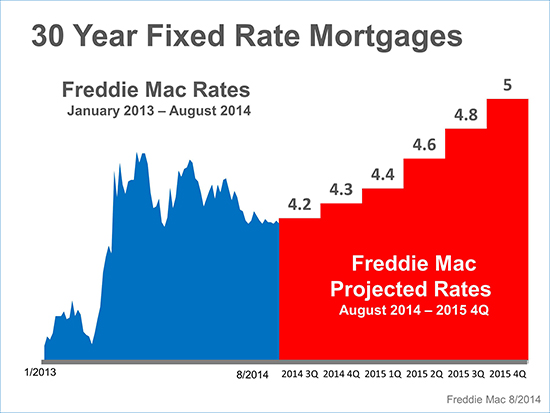

From ACAR Watercooler

by Marc Lebowitz, RCE, CAE

ACAR Executive Director

Single family home sales in July 2014 were 832 in Ada County, a decrease of 7% compared to July 2013. YTD total sales are down 3% compared to this time last year; 4,525 homes sold compared to 4,674.

In July 78% of our total sales were for homes priced above $160,000.

In July sales of homes in the $160,000 - $200,000 were up 18% from June 2014 to 194. This category had the greatest sales increase month-over-month and was the highest sales category behind. Sales in price points above $200,000 cooled slightly in July

Days on Market for July were 47; one day more than last month. In July 2013, Days on Market was 44.

New homes sold in July totaled 156; down 5% from last year; up 3% over June.

Existing home sales were 676; down 8% from July 2013.

Historically July sales fall off from June levels. Last year and this year the trend has been reversed. July 2013 increased over June 2013 by 9%. July 2014 increased over June 2104 by 4%.

July 2013 was the peak in a very strong sales year. Although we’ve had four consecutive months with sales behind the previous year, our sales trend for 22014 is strong.

Pending sales at the end of July were 988; down 20% from July 2013. Pending sales have trailed behind previous year’s pending sales for twelve consecutive months.

July median home price was $213,800; up 3% from July 2013. Our YTD median price is $208,729; up 7% over last year.

New Homes median price for July was $311,540; up 16% from July 2013. For Existing homes the increase is 3% to $195,000.

The number of houses available for sale at the end of July increased 4% from June 2014 to 2,907. This is an increase we really need. This is 14% more than last year at this time.

We anticipate continued inventory growth from now until the end of Summer.

The price point with the largest increase month-over-month is $160,000 - $200,000 at 7%. The next highest is $120,000 - $160,000 with 6%.

In Ada County we now have 3.6 months of inventory on hand, essentially unchanged from the end of June.

The price categories in shortest supply are $120,000 to $160,000 which has 2.1 months; and $100,000 - $119,000 which has 2.2 months.

From $160,000 to $400,000 we have 3.6 months; not much change from last month.

Of sales in July, the most popular price point was $160,000 to $200,000 (23%); and $120,000 to $160,000 (18%) followed by $200,000 - $300,000 with 16%.

So…what’s next?

We’ve compared pretty well to 2013 for the first seven months of 2014. From now until December we should trend ahead of 2013 sales and median should hold steady.

We have more inventory coming online in the <$160,000 which will release some pent up demand among first time buyers.

Median price shows no signs of weakening.

Boise was named the “Best City to Move to in 2104” last week because of our ‘Median Income” “Home Value Growth” and “Home Affordability”.

All in all, I’m still feeling pretty good about how we will finish the year.

The safest drivers in America, for the fourth year in a row, hail from

The safest drivers in America, for the fourth year in a row, hail from  Drivers in the city of 150,000 north of Denver can expect to go 14.2 years between accidents, according to the insurance giant’s claims data. Contrast that with 200th-ranked Worcester, Massachusetts, where drivers go just 4.3 years between claims.

Drivers in the city of 150,000 north of Denver can expect to go 14.2 years between accidents, according to the insurance giant’s claims data. Contrast that with 200th-ranked Worcester, Massachusetts, where drivers go just 4.3 years between claims.