New guideline released by HUD may result in you being able to buy a house again sooner ranter than later. I am including a introduction below. If you think this might help you, contact me for a good lender to consult with.

HUD recently announced that people who lost their home through a foreclosure, short sale or bankruptcy, may be eligible to finance a home again in as little as 12 months. This is a reduction from the previously required minimum of 36 months from the date of the “most recent event.”

Released August 15, HUD provided guidelines under

“Back to Work – Extenuating Circumstances” meant to ease the path for home ownership for many.

Boomerang homebuyers, as they are now known, will need to document that the reason they were unable to make their payments was due to a specific Economic Event. This impact of this event must have resulted in a decline in income of 20% or more for at least six months.

Some boomerang homebuyers who experienced a bankruptcy and simultaneous foreclosure have discovered that the two events may not be recorded at the same time. In cases where the property did not transfer back to the lender at the time of the bankruptcy, the period for the 36 month minimum waiting period as was required by HUD, did not start until the title transferred back to the lender. In some states, the time for transfer could be months or even years after the discharge of the bankruptcy.

Extenuating Circumstances

Extenuating circumstances for the purpose of these guidelines are as follows. The borrower(s) must have experienced a decline in income of 20% or more for a period of at least six months. This could have been due to a job loss or a loss of income tied to earnings like commissions or other customary bonus or incentive income.

Demonstrated Cure

With any situation of extenuating circumstances, a boomerang homebuyer must be able to document that the event was isolated in nature and not likely to reoccur again in the future. The borrower must also be able to document that they have regained economic stability through timely payments for a minimum of 12 months.

The timely payment history will include rental/mortgage payments, installment payments, and/or revolving payments for the 12 months preceding the mortgage application. There also should not be any new collection accounts.

In addition to re-establishing acceptable credit, the borrower(s) will be required to complete Housing Counseling.

Eligibility Requirements for Documenting Loss of Income

In the event of a loss in employment, the lender will need to document the event by a written Verification of Employment evidencing the termination date, public information documenting the closure of the business if applicable and/or documentation of unemployment income.

The lender will also need to substantiate the loss of income through the verification of tax returns, W-2s and tax transcripts.

Important Definitions

HUD announced several key terms that must be reviewed in accordance with this program.

Economic Event: an occurrence beyond the borrowers control that resulted in a Loss of Employment, Loss of Income or a combination of both which resulted in a loss of Household Income of 20% or more for a period of six or more months.

Onset of Economic Event: the month of the start of or loss of income

Recovery from an Economic Event: the re-establishment of acceptable or satisfactory credit. Satisfactory Credit equates to no derogatory credit for any mortgaged or leased property in the 12 months preceding the mortgage application. This also includes any installment or revolving debt for the same period.

Borrower: “Borrower” includes all parties including primary and/or co-borrower as listed on the loan application.

Borrower Household Income: the income of all parties on the application or Household Members as listed from the previous Economic Event and derogatory credit.

Housing Counseling: Counseling from a HUD-approved housing counseling agency related to home ownership and meets acceptable requirements.

Other Requirements and Information

HUD establishes a base line for lenders to underwrite and approve mortgage applications. Some lenders may choose to require baseline standards that exceed the minimum guidelines listed here with regards to time from short sale, foreclosure or bankruptcy.

Lenders may also choose to enact additional overlays with requirements to evaluation acceptable credit regarding payment history, collection accounts and/or judgments.

In the event a prior defaulted mortgage was endorsed by FHA, the lender will need to request a waiver which may require additional time for processing. For anyone this pertains to, they would be wise to alert the new lender to this as soon as possible in the loan process.

Boomerang homebuyers whose prior hardship was economically driven should be excited by this announcement from HUD. For many, it is now recognized the worst is behind them and the time to buy a new home is here.

Eric Belsky is Managing Director of the Joint Center of Housing Studies at Harvard University. He also currently serves on the editorial board of the Journal of Housing Research and Housing Policy Debate. This year he released a new paper on homeownership -

Eric Belsky is Managing Director of the Joint Center of Housing Studies at Harvard University. He also currently serves on the editorial board of the Journal of Housing Research and Housing Policy Debate. This year he released a new paper on homeownership -  The fixer-upper properties on the market will give you more purchasing power when shopping for a new home. Bargains can be found in homes that have been foreclosed, seized by the government or just fallen out of repair due to homeowner neglect. While it is true that you will save thousands of dollars on these homes that will need lots of work, there are hidden costs that buyers fail to consider. Ask yourself if it’s worth it and know your options.

The fixer-upper properties on the market will give you more purchasing power when shopping for a new home. Bargains can be found in homes that have been foreclosed, seized by the government or just fallen out of repair due to homeowner neglect. While it is true that you will save thousands of dollars on these homes that will need lots of work, there are hidden costs that buyers fail to consider. Ask yourself if it’s worth it and know your options.

There are some homeowners that might consider waiting for the spring to sell their house thinking that no one buys a home during the winter months. What we should understand is that homes sell EVERY DAY. As a matter of fact, according to the latest

There are some homeowners that might consider waiting for the spring to sell their house thinking that no one buys a home during the winter months. What we should understand is that homes sell EVERY DAY. As a matter of fact, according to the latest  Many sellers feel that the spring is the best time to place their home on the market as buyer demand increases at that time of year. However, the fall and winter have their own advantages. Here are five reasons to sell now.

Many sellers feel that the spring is the best time to place their home on the market as buyer demand increases at that time of year. However, the fall and winter have their own advantages. Here are five reasons to sell now.

One of the first stages during the hunt for a new home is crunching the numbers to figure out your budget. And no matter how high or low that budget may be, prospective homebuyers should take into consideration the cost of insuring the home.

One of the first stages during the hunt for a new home is crunching the numbers to figure out your budget. And no matter how high or low that budget may be, prospective homebuyers should take into consideration the cost of insuring the home.

As we enter the winter months, many expect the real estate market to begin to slow down. However, this winter there are many reasons that both buyers and sellers should consider moving forward with their real estate goals instead of waiting until the spring.

As we enter the winter months, many expect the real estate market to begin to slow down. However, this winter there are many reasons that both buyers and sellers should consider moving forward with their real estate goals instead of waiting until the spring.

Even though no one at KCM actively lists or sells real estate, some of our readers believe that there is an inherent basis toward the real estate community in our writing. For that reason, we want to quote a third party source today.Forbes, in their online edition last week, spoke to the importance of buying a home now rather than waiting.

Even though no one at KCM actively lists or sells real estate, some of our readers believe that there is an inherent basis toward the real estate community in our writing. For that reason, we want to quote a third party source today.Forbes, in their online edition last week, spoke to the importance of buying a home now rather than waiting.

![CoffeeInfographic-e1379346654723[1]](http://www.kcmblog.com/wp-content/uploads/2013/09/StarbucksInfographic-e13793466547231.jpg)

The shortage of homes for sale earlier in the year created an imbalance of supply to demand which resulted in double digit year-over-year price increases nationally. According to a recent Wall Street Journal

The shortage of homes for sale earlier in the year created an imbalance of supply to demand which resulted in double digit year-over-year price increases nationally. According to a recent Wall Street Journal  Many now realize that it is a great time to buy a home. Today, we want to look at why it might also be an opportune time to sell your house. Here are the Top 5 Reasons we believe now may be a perfect time to put your house on the market.

Many now realize that it is a great time to buy a home. Today, we want to look at why it might also be an opportune time to sell your house. Here are the Top 5 Reasons we believe now may be a perfect time to put your house on the market. There are some homeowners that have been waiting for months to get a price they hoped for when they originally listed their house for sale. The only thing they might want to consider is…

There are some homeowners that have been waiting for months to get a price they hoped for when they originally listed their house for sale. The only thing they might want to consider is…

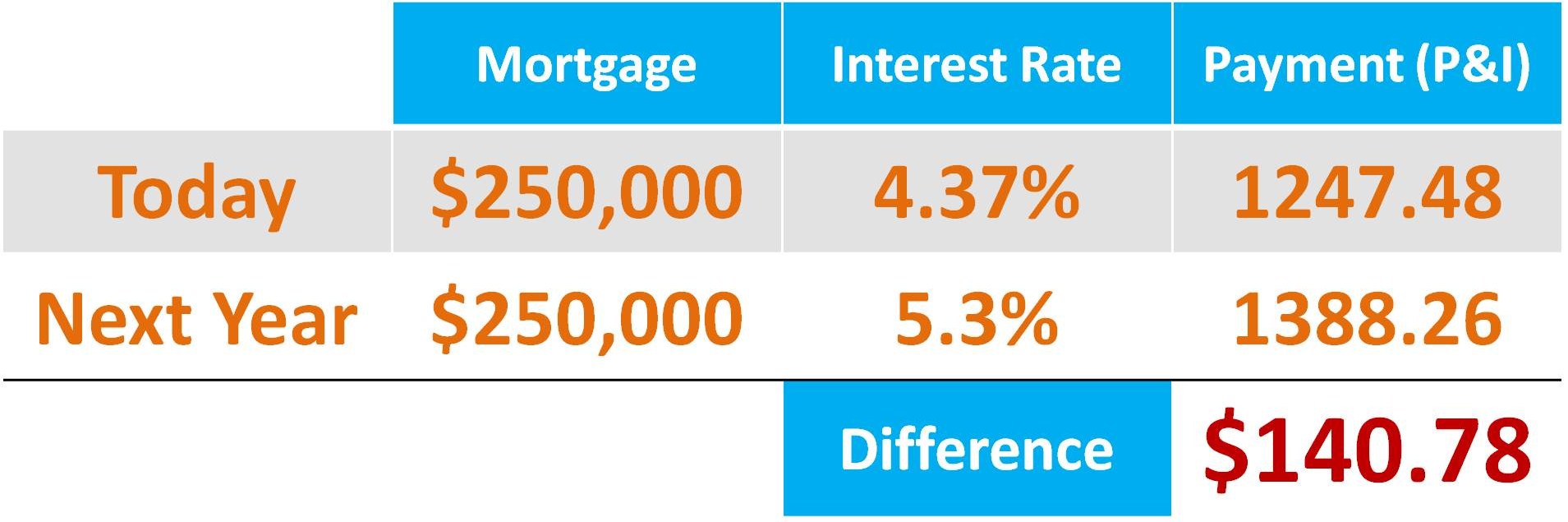

The cost of a home is determined mainly by two components: price and mortgage rate. Today, we want to show how the monthly cost of purchasing a median priced home has changed over the last twelve months and how it might change over the next twelve months. For the first two examples, we will be using the National Association of Realtors’ (NAR) Existing Home Sales Report to establish median price and Freddie Mac’s Primary Mortgage Market Survey to establish mortgage rate. We also assumed a 20% down payment in all examples.

The cost of a home is determined mainly by two components: price and mortgage rate. Today, we want to show how the monthly cost of purchasing a median priced home has changed over the last twelve months and how it might change over the next twelve months. For the first two examples, we will be using the National Association of Realtors’ (NAR) Existing Home Sales Report to establish median price and Freddie Mac’s Primary Mortgage Market Survey to establish mortgage rate. We also assumed a 20% down payment in all examples.