In a recent blog post, FreddieMac explained that “housing is stronger today than at any point since the Great Recession began and hit bottom in 2009”. They then gave three reasons which support their position: In a recent blog post, FreddieMac explained that “housing is stronger today than at any point since the Great Recession began and hit bottom in 2009”. They then gave three reasons which support their position:

Projections Going ForwardFreddieMac also believes that the market will continue to improve through 2014. They projected:

Frank Nothaft, Freddie Mac vice president and chief economist, further explained what the housing market may look like in the agency’s April 2014 U.S. Economic and Housing Market Outlook: "Tight inventory may pose a significant challenge for home buyers in many markets across the country, which may result in higher home prices and sales being lower than expected. This is good news for those markets that have room to run on the house price appreciation front, but it's also going to increase the affordability pinch in many markets, especially along the country's east and west coasts. Two indicators that are supporting local housing activity are rising consumer confidence and declining unemployment rates." Bottom LineThe real estate market is improving every day. The biggest challenge is a lack of inventory in many markets. If you are thinking about selling, now may be the time to make the move. |

Wednesday, April 30, 2014

Freddie Mac: Housing is Stronger Today

Tuesday, April 29, 2014

Does staging raise a home's sale price?

Does staging raise a home's sale price?

One study says staging doesn't affect value. Here's why real estate agents disagree. By Michael Estrin, Bankrate.com

By Michael Estrin, Bankrate.com

• Might not be as important as many real estate agents think.

• Likely doesn't raise the home's sale price.

Study used virtual tours on computers

The study surveyed 820 homebuyers, walking them through a series of six virtual tours of a single home. Each tour focused on either wall color or furnishings, which are two of the most popular staging elements, according to study co-author Michael Seiler, professor of real estate and finance at the College of William & Mary.

In one virtual tour, the buyers saw the home without furniture.

- In another virtual tour, they saw the same property, but with "ugly" furniture.

- In yet another virtual tour, they saw the same property, but with "good" furniture.

- The wall color variations included a neutral beige and an "unattractive" purple.

Ugly didn't matter

As it turned out, neither wall color nor furnishings made much of an impact on the potential sale price. According to the study, buyers were willing to pay the same price, about $204,000, regardless of how the property was staged.

- "(Staging) choices do not appear to have a significant effect on the actual revealed market value of the property," the study's authors wrote. "These results stand in stark contrast to the conscious opinion of both buyers and real estate agents that staging conditions significantly impact willingness to pay for a home."

The study is titled "The Impact of Staging Conditions on Residential Real Estate Demand." Its co-authors are Mark Lane, associate professor in the finance department at Old Dominion University, and Vicky Seiler, researcher at Johns Hopkins University.

Why staging didn't matter

One reason staging may not help raise the price, according to Seiler, is that buyers are savvy. They know that staging is a superficial process, he says, and they know that cosmetic changes don't cost much.

- The same potential buyers thought that other buyers would spend more on the properties in the tour, which may explain why we don't question the wisdom of staging.

"In individuals, there's often a difference between the stated preference and the revealed preference," he says.

The upside to staging

While sellers may not like hearing that money spent on staging won't yield a higher price, Seiler says, "I am definitely not ready to say spending money on staging would be a waste."

- For one thing, the study found that staging does give buyers a more favorable impression of the home's livability, something Seiler says he believes may help the property sell faster. He says the study might not be applicable to all price points and locations.

"It seems plausible that different clientele might be differentially influenced by staging," he says. "It also seems reasonable to suspect different staging looks would appeal to different tastes and preferences of people."

Advantages of staging

"Staging is a must," says Alexis Moore, a broker for Blackstone Realty Group in El Dorado Hills, Calif. "Most sellers don't want to spend the money. But they should because, in the end, it is well worth it."

According to Moore, staging gives sellers two competitive advantages:

- Staging allows the seller to turn a potential negative into a positive.

- Buyers are picky, which means a well-staged home will stand out in the market.

By contrast, Moore says an unstaged home could stick out, but not in ways that attract buyers.

Staging as another tool

There are also plenty of agents such as Betty-Jo Tilley, a luxury-home specialist with Berkshire Hathaway HomeServices in Los Angeles, who say staging has helped them raise the sale price. But price mostly is defined by comparable listings, which means staging is one of many tools that can help sellers hit their target.

- "The highest-priced sales of comparable homes in the area reveal a great deal about what will satisfy potential homebuyers," Tilley says. "Those homes can be used as a target, depending on the amount of staging that the owner is willing to do."

Price versus days on market

Not all real estate agents disagree with the study's findings in theory.

"Staging a home greatly improves its showability, therefore making it much more likely to sell," says David Buck, owner of Coldwell Banker Lota Realty in Taos, N.M. "But it's difficult to necessarily translate that into a higher price -- only fewer days on the market."

Still, for Buck, staging remains an essential part of marketing a home, especially in a buyer's market.

"In a market with a lot of unsold inventory, staging certainly perks up a property and separates it from a cold, vacant listing," Buck says.

Monday, April 28, 2014

The State of Hispanic Homeownership

Courtesy of KCM Blog

This month the National Association of Hispanic Real Estate Professionals (NAHREP) released their annual State of Hispanic Homeownership Report for 2013. A 35 page report designed to highlight “the homeownership growth and household formation rates of Hispanics as well as their educational achievements, entrepreneurial endeavors, labor force profile, and purchasing power in the United States”.

This month the National Association of Hispanic Real Estate Professionals (NAHREP) released their annual State of Hispanic Homeownership Report for 2013. A 35 page report designed to highlight “the homeownership growth and household formation rates of Hispanics as well as their educational achievements, entrepreneurial endeavors, labor force profile, and purchasing power in the United States”.

This report is full of great information and you should download it and read all 35 pages. In this blog post, I will mention a few facts that, in my opinion, are relevant to all of us:

Household formation

Hispanic Millennials

Income

The Hispanic community is becoming a major player in the housing market.

This month the National Association of Hispanic Real Estate Professionals (NAHREP) released their annual State of Hispanic Homeownership Report for 2013. A 35 page report designed to highlight “the homeownership growth and household formation rates of Hispanics as well as their educational achievements, entrepreneurial endeavors, labor force profile, and purchasing power in the United States”.This report is full of great information and you should download it and read all 35 pages. In this blog post, I will mention a few facts that, in my opinion, are relevant to all of us:

Household formation

- Since 2010, Hispanics have accounted for a net increase of 559,000 owner households, representing 56 percent of the total net growth of owner households in the U.S.

- The number of Hispanic households has grown from 9.2 million in 2000 to 14.7 million in 2013, an increase of 5.5 million, representing a growth rate of 60 percent.

- Four out of 10 new households between 2010 and 2020 are expected to be Hispanic.

- By the end of the decade, Hispanics alone will account for approximately five million net new households, out of an estimated 12 to 14 million net new households in the country.

Hispanic Millennials

- The median age of the Hispanic population is 27 years old, which is ten years younger than the median age of the overall U.S. population.

- Hispanics are heavily represented in the 26 to 46 year age range.

- A Hispanic youth turns 18 every minute of every day.

Income

- Hispanics with incomes between $50,000 and $100,000 represent 29 percent of all Hispanic households and comprise nearly 40 percent of Hispanic purchasing power.

- Three out of every four prosperous Hispanics are under the age of 45 and own a home.

- Twenty-two percent of all Hispanic households earn more than $75,000 annually.

- The number of Hispanic-owned businesses in the U.S. nearly doubled from more than a decade ago, growing from 1.7 million in 2002 to an estimated 3.2 million in 2013.

- Latina entrepreneurs are launching businesses at a rate SIX TIMES the national average.

- Hispanic businesses contribute in excess of $465 billion to the nation’s economy annually and employ more than two million workers.

- Latinos now own one out of every 20 businesses in the U.S., while Latinas own 10 percent of all women-owned businesses.

The Hispanic community is becoming a major player in the housing market.

Saturday, April 26, 2014

Friday, April 25, 2014

March Market Report: Daffodils and Sunshine!

As a follow-up from yesterday's Ada County Market Report by Ada County Association of Realtors here are some related graphs. (For you visual types out there.)

Median Price

Single Family Home Sales

Single Family Home Sales

Active Inventory

Active Inventory

Median Price

Single Family Home SalesActive Inventory

Thursday, April 24, 2014

Strongest March since 2007!

March Market Report:Daffodils and Sunshine

April 11, 2014 by Marc Lebowitz · Leave a Comment

Single family home sales in March 2014 were 580 in Ada County, an increase of 4% compared to March 2013. YTD total sales are up 2% compared to this time last year; 1,425 homes sold compared to 1,396.

March 2014 is the strongest March we’ve had since 2007.

In March 60% of our total sales were for homes priced above $160,000. This graphically portrays the diminishing role that fist –time buyers has on our market. In 2010 more than 52% of buyers were “first-time”. Today the number of first-time buyers is closer to 35%. Long-term this is could become problematic for the large number of millennials wanting to more from renters to owners.

Days on Market for March were 67. That’s about the same as in February, but still up significantly from December’s 59. In March 2013, Days on Market was 66.

New homes sold in March totaled 112; down 17% from last year.

Existing home sales were 468; up 10%.

Historically, March sales increase from February by an average of 36%. March 2014 posted a 37% increase over February.

Of the total sales in March, 12% were distressed; down 1% from last month. In March 2013, 17% of sales were distressed.

For the month of March, REO sales (60% of Distressed; 34 total sales) exceeded Short Sales (40% of Distressed; 24 total sales).

Pending sales at the end of March were 1078; down 16% from March 2013. Pending sales have traied behind previous year’s pending sales for eight consecutive months.

Of Pending sales in distress (11%), there are slightly more Short Sales (54%; 59 sales) than REO’s (46%; 50 sales).

March median home price was $197,900; up 5% from March 2013. Our YTD median price is $200,000; up 8% over last year.

New Homes median price for March was $300,884; up 19% from March 2013. For Existing homes the increase is 7% to $181,125.

The number of houses available for sale at the end of March increased 5% from February 2014 to 2,246. This is an increase we really needed going into Spring selling season. This is 25% more than last year at this time.

We anticipate continued inventory growth from now until the end of Summer.

Of the total active listings, 8% are distressed, down 2% from February.

Of our Distressed Inventory, 66% is Short Sales (118) and 34% is REO (61).

In Ada County we now have 4.5 months of inventory on hand, down a little from the end of February.

The price category in shortest supply is <$100K where we have 1.2 months.

From $100,000 to $119,000 we have 1.6 months available.

From $120,000 to $160,000 we have just under 3 months available inventory.

From $160,000 to $300,000 we have nearly 5 months…except for the very popular $250,000 – $300,000 which has only 4.6 month’s supply available.

Above $300,000 we have a 6 month’s supply. Above $500,000 the supply is closer to 22 months. Remembering that 6 months of available inventory describes a “stable real estate market”; it looks like we are heading into a period of “normal” like we haven’t seen in several years.

Of sales in March, the most popular price point was $120,000 to $160,000 (24%); followed by $160,000 to $200,000 (21%) and $200,000 to $250,000 with 14%.

So…what’s next?

Sales in March were jump started from February. We are now chasing a super strong Spring and Summer 2013. April 2013 sales were 719. Can we increase sales from 580 to 719 with Pending sales where they are? It’s going to be very close.

March is typically a bellwether month for sales and median home price. March 2014 was pretty strong in both categories. This should continue into the Summer.

We are seeing more and more data that says that the Millennials (the big homebuyer wild card) are feeling better and better about home ownership. Nearly 90% of Millennial buyers say “homeownership is a good investment”. Our problem is that we don’t have enough inventory to pull them out of their apartments and into homes

This is the pent up demand we’ve been waiting to see activate.

Bottom line…its going to be a roller coaster summer.

March 2014 is the strongest March we’ve had since 2007.

In March 60% of our total sales were for homes priced above $160,000. This graphically portrays the diminishing role that fist –time buyers has on our market. In 2010 more than 52% of buyers were “first-time”. Today the number of first-time buyers is closer to 35%. Long-term this is could become problematic for the large number of millennials wanting to more from renters to owners.

Days on Market for March were 67. That’s about the same as in February, but still up significantly from December’s 59. In March 2013, Days on Market was 66.

New homes sold in March totaled 112; down 17% from last year.

Existing home sales were 468; up 10%.

Historically, March sales increase from February by an average of 36%. March 2014 posted a 37% increase over February.

Of the total sales in March, 12% were distressed; down 1% from last month. In March 2013, 17% of sales were distressed.

For the month of March, REO sales (60% of Distressed; 34 total sales) exceeded Short Sales (40% of Distressed; 24 total sales).

Pending sales at the end of March were 1078; down 16% from March 2013. Pending sales have traied behind previous year’s pending sales for eight consecutive months.

Of Pending sales in distress (11%), there are slightly more Short Sales (54%; 59 sales) than REO’s (46%; 50 sales).

March median home price was $197,900; up 5% from March 2013. Our YTD median price is $200,000; up 8% over last year.

New Homes median price for March was $300,884; up 19% from March 2013. For Existing homes the increase is 7% to $181,125.

The number of houses available for sale at the end of March increased 5% from February 2014 to 2,246. This is an increase we really needed going into Spring selling season. This is 25% more than last year at this time.

We anticipate continued inventory growth from now until the end of Summer.

Of the total active listings, 8% are distressed, down 2% from February.

Of our Distressed Inventory, 66% is Short Sales (118) and 34% is REO (61).

In Ada County we now have 4.5 months of inventory on hand, down a little from the end of February.

The price category in shortest supply is <$100K where we have 1.2 months.

From $100,000 to $119,000 we have 1.6 months available.

From $120,000 to $160,000 we have just under 3 months available inventory.

From $160,000 to $300,000 we have nearly 5 months…except for the very popular $250,000 – $300,000 which has only 4.6 month’s supply available.

Above $300,000 we have a 6 month’s supply. Above $500,000 the supply is closer to 22 months. Remembering that 6 months of available inventory describes a “stable real estate market”; it looks like we are heading into a period of “normal” like we haven’t seen in several years.

Of sales in March, the most popular price point was $120,000 to $160,000 (24%); followed by $160,000 to $200,000 (21%) and $200,000 to $250,000 with 14%.

So…what’s next?

Sales in March were jump started from February. We are now chasing a super strong Spring and Summer 2013. April 2013 sales were 719. Can we increase sales from 580 to 719 with Pending sales where they are? It’s going to be very close.

March is typically a bellwether month for sales and median home price. March 2014 was pretty strong in both categories. This should continue into the Summer.

We are seeing more and more data that says that the Millennials (the big homebuyer wild card) are feeling better and better about home ownership. Nearly 90% of Millennial buyers say “homeownership is a good investment”. Our problem is that we don’t have enough inventory to pull them out of their apartments and into homes

This is the pent up demand we’ve been waiting to see activate.

Bottom line…its going to be a roller coaster summer.

Tuesday, April 22, 2014

Either Way, You're Still Paying A Mortgage!

There are some people that have not purchased a home because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that, unless you are living with our parents rent free, you are paying a mortgage - either your mortgage or your landlord’s.

There are some people that have not purchased a home because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that, unless you are living with our parents rent free, you are paying a mortgage - either your mortgage or your landlord’s.As a recent paper from the Joint Center for Housing Studies at Harvard University explains:

“Households must consume housing whether they own or rent. Not even accounting for more favorable tax treatment of owning, homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord plus a rate of return. That’s yet another reason owning often does—as Americans intuit—end up making more financial sense than renting.”

Also, if you purchase with a 30-year fixed rate mortgage, your ‘housing expense’ is locked in over the thirty years for the most part. If you rent, the one guarantee you will have is that your rent will increase over that same thirty year time period.

Whether you are looking for a primary residence for the first time or are considering a vacation home on the shore, owning might make more sense than renting since prices and interest rates are still at bargain prices.

Monday, April 21, 2014

PTC Index for March

PTC Index – March 2014

The spring buying season was off to a good start in March with the PTC Index showing encouraging gains and losses in most categories from the month before. First, building permits remained unchanged from the month prior, settling at 258 filings; building permits are down slightly from a year ago by roughly 16 percent. Although new home sales are down by nine percent from a year ago as well, we saw a 21 percent jump from February. Existing home sales surged in March by about 44 percent from the month prior; existing home sales are up about 9 percent from March 2013. Refinance activity made its first increase since November, inching up slightly by 1.7 percent, though still down 52 percent from a year ago. The average sales price also made its first rebound since October 2013 climbing 3.3 percent from February 2014. Finally, both notices of default and distressed properties decreased in March from the month before by 13.7 percent and 8.1 percent, respectively. In the year-ago time period, these categories are also down by 24 percent and 42.3%, respectively.

For comparison, index was 130 in January and 132 in February.

The spring buying season was off to a good start in March with the PTC Index showing encouraging gains and losses in most categories from the month before. First, building permits remained unchanged from the month prior, settling at 258 filings; building permits are down slightly from a year ago by roughly 16 percent. Although new home sales are down by nine percent from a year ago as well, we saw a 21 percent jump from February. Existing home sales surged in March by about 44 percent from the month prior; existing home sales are up about 9 percent from March 2013. Refinance activity made its first increase since November, inching up slightly by 1.7 percent, though still down 52 percent from a year ago. The average sales price also made its first rebound since October 2013 climbing 3.3 percent from February 2014. Finally, both notices of default and distressed properties decreased in March from the month before by 13.7 percent and 8.1 percent, respectively. In the year-ago time period, these categories are also down by 24 percent and 42.3%, respectively.

March 2014

| Building Permits | 258 |

| New Home Sales | 153 |

| Existing Home Sales | 680 |

| Refinance | 641 |

| Average Sales Price | 191027.5 |

| Financial-Bond Market(10-yr Treasury) | 2.72 |

| Days on Market | 66 |

| Distressed(Short Sales and REO) | 1063 |

| Notices of Default | 139 |

| PTC Index | 168 |

For comparison, index was 130 in January and 132 in February.

Wednesday, April 16, 2014

Really? Granite countertops, stainless steel appliances still popular

Making minor improvements to homes rather than full-on remodeling is the most cost-effective way for sellers to boost the value of their properties, according to Zillow.

Real estate agents and interior designers who responded to a survey from Zillow’s home improvement marketplace, Zillow Digs, said that low-cost projects like landscaping and painting walls in neutral colors offer sellers more bang for their buck than full-blown renovations, whose addition to a home’s value might not outweigh their cost.

According to the survey, the five home improvement projects delivering the most bank for the buck are:

Most high-end finishes “don’t equal high-end returns,” says Zillow Agent Advisory Board member Bic DeCaro of Westgate Realty Group in Falls Church, Va. Interior design trends come and go. But most buyers are still requesting granite countertops and stainless steel appliances, DeCaro said.

- See more at: http://www.inman.com/2014/04/10/really-granite-countertops-stainless-steel-appliances-still-popular-with-homebuyers/#sthash.RpjN7eHK.dpuf

Real estate agents and interior designers who responded to a survey from Zillow’s home improvement marketplace, Zillow Digs, said that low-cost projects like landscaping and painting walls in neutral colors offer sellers more bang for their buck than full-blown renovations, whose addition to a home’s value might not outweigh their cost.

According to the survey, the five home improvement projects delivering the most bank for the buck are:

- Curb appeal (fresh potted flowers, a fresh coat of paint on the front door).

- Staging (“neutral colors and minimal furniture are best”).

- Small home improvements (updated lighting fixtures, cabinet or door handles, and minor kitchen and bathroom updates).

- Decluttering (“Old appliances and furniture can be overlooked if a space is clean, simple and well-edited.”)

- Granite countertops and stainless steel appliances.

Most high-end finishes “don’t equal high-end returns,” says Zillow Agent Advisory Board member Bic DeCaro of Westgate Realty Group in Falls Church, Va. Interior design trends come and go. But most buyers are still requesting granite countertops and stainless steel appliances, DeCaro said.

- See more at: http://www.inman.com/2014/04/10/really-granite-countertops-stainless-steel-appliances-still-popular-with-homebuyers/#sthash.RpjN7eHK.dpuf

Tuesday, April 15, 2014

Want to Sell Your House? Price it Right!

The housing market is recovering nicely. Prices have increased nationally by double digits over the last twelve months. Competition from the shadow inventory of lower priced distressed properties (foreclosures and short sales) is diminishing rapidly. Now may be the perfect time to sell your home and move to the dream house or beautiful location your family has always talked about.

The housing market is recovering nicely. Prices have increased nationally by double digits over the last twelve months. Competition from the shadow inventory of lower priced distressed properties (foreclosures and short sales) is diminishing rapidly. Now may be the perfect time to sell your home and move to the dream house or beautiful location your family has always talked about.The one suggestion we would definitely offer: DON’T OVERPRICE IT!!

Even though prices have increased by more than 10% over the last year, the acceleration of appreciation has slowed dramatically over the last few months. As an example, in their April Home Price Index Report, CoreLogic revealed that home prices actually depreciated by .08% this month as compared to last month’s report. What concerns us is that Trulia just reported that asking prices are still continuing to increase.

Because investor purchases are declining and there are more listings coming onto the market, we believe that sellers should be very cautious when they price their house. The alternative might be that you could lose money by overpricing your home at the start as explained in aresearch study on the matter.

Bottom Line

Though it is a great time to sell your house, pricing it right is crucial. Get guidance from a real estate professional in your marketplace to ensure you get the best deal possible.

Sunday, April 13, 2014

Idaho Vacancies Have Hit Record Lows in 2014

Now is good time to look at purchasing rental property!

Mountain States Appraisal surveyed over 13,000 apartment units in Ada County in January, and the numbers may surprise you. With demand way above supply this may be the perfect opportunity to pitch investors to invest in Idaho where the vacancy rate is the lowest in the country. Look below to see how vacancies have dropped 7 percentage points in the last 5 years.

numbers may surprise you. With demand way above supply this may be the perfect opportunity to pitch investors to invest in Idaho where the vacancy rate is the lowest in the country. Look below to see how vacancies have dropped 7 percentage points in the last 5 years.

Vacancy Overview

Mountain States Appraisal surveyed over 13,000 apartment units in Ada County in January, and the

numbers may surprise you. With demand way above supply this may be the perfect opportunity to pitch investors to invest in Idaho where the vacancy rate is the lowest in the country. Look below to see how vacancies have dropped 7 percentage points in the last 5 years.| Units Surveyed | Reported Vacancy | Vacancy By Bedroom Count | |||

| 1 BR | 2 BR | 3 BR | |||

| January-2014 | 13,933 | 2.3% | 1.6% | 2.9% | 2.6% |

| January-2013 | 13,788 | 4.0% | 3.6% | 4.1% | 6.0% |

| January -2012 | 13,689 | 4.5% | 4.0% | 4.6% | 6.3% |

| January -2011 | 13,689 | 5.7% | 5.6% | 5.9% | 5.8% |

| January -2010 | 13,294 | 9.4% | 7.3% | 10.5% | 13.6% |

| January -2009 | 13,288 | 9.5% | 7.9% | 10.3% | 11.7% |

| January- 2008 | 13,413 | 5.6% | 4.9% | 5.8% | 7.2% |

| January- 2007 | 13,456 | 4.2% | 3.2% | 4.7% | 6.4% |

| January -2006 | 14,113 | 6.9% | 6.1% | 7.3% | 9.7% |

| January -2005 | 13,659 | 8.5% | 6.4% | 8.8% | 14.6% |

Saturday, April 12, 2014

Ada County Market Report for March

| March Market Report…its all Daffodils and Sunshine…for now.by marclebowitz |

by Marc Lebowitz, RCE, CAE

ACAR Executive Director

Single family home sales in March 2014 were 580 in Ada County, an increase of 4% compared to March 2013. YTD total sales are up 2% compared to this time last year; 1,425 homes sold compared to 1,396.

March 2014 is the strongest March we’ve had since 2007.

In March 60% of our total sales were for homes priced above $160,000. This graphically portrays the diminishing role that fist –time buyers has on our market. In 2010 more than 52% of buyers were “first-time”. Today the number of first-time buyers is closer to 35%. Long-term this is could become problematic for the large number of millennials wanting to more from renters to owners.

Days on Market for March were 67. That’s about the same as in February, but still up significantly from December’s 59. In March 2013, Days on Market was 66.

New homes sold in March totaled 112; down 17% from last year.

Existing home sales were 468; up 10%.

Historically, March sales increase from February by an average of 36%. March 2014 posted a 37% increase over February.

Of the total sales in March, 12% were distressed; down 1% from last month. In March 2013, 17% of sales were distressed.

For the month of March, REO sales (60% of Distressed; 34 total sales) exceeded Short Sales (40% of Distressed; 24 total sales).

Pending sales at the end of March were 1078; down 16% from March 2013. Pending sales have traied behind previous year’s pending sales for eight consecutive months.

Of Pending sales in distress (11%), there are slightly more Short Sales (54%; 59 sales) than REO’s (46%; 50 sales).

March median home price was $197,900; up 5% from March 2013. Our YTD median price is $200,000; up 8% over last year.

New Homes median price for March was $300,884; up 19% from March 2013. For Existing homes the increase is 7% to $181,125.

The number of houses available for sale at the end of March increased 5% from February 2014 to 2,246. This is an increase we really needed going into Spring selling season. This is 25% more than last year at this time.

We anticipate continued inventory growth from now until the end of Summer.

Of the total active listings, 8% are distressed, down 2% from February.

Of our Distressed Inventory, 66% is Short Sales (118) and 34% is REO (61).

In Ada County we now have 4.5 months of inventory on hand, down a little from the end of February.

The price category in shortest supply is <$100K where we have 1.2 months.

From $100,000 to $119,000 we have 1.6 months available.

From $120,000 to $160,000 we have just under 3 months available inventory.

From $160,000 to $300,000 we have nearly 5 months…except for the very popular $250,000 – $300,000 which has only 4.6 month’s supply available.

Above $300,000 we have a 6 month’s supply. Above $500,000 the supply is closer to 22 months. Remembering that 6 months of available inventory describes a “stable real estate market”; it looks like we are heading into a period of “normal” like we haven’t seen in several years.

Of sales inMarch, the most popular price point was $120,000 to $160,000 (24%); followed by $160,000 to $200,000 (21%) and $200,000 to $250,000 with 14%.

So…what’s next?

Sales in March were jump started from February. We are now chasing a super strong Spring and Summer 2013. April 2013 sales were 719. Can we increase sales from 580 to 719 with Pending sales where they are? It’s going to be very close.

March is typically a bellwether month for sales and median home price. March 2014 was pretty strong in both categories. This should continue into the Summer.

We are seeing more and more data that says that the Millennials (the big homebuyer wild card) are feeling better and better about home ownership. Nearly 90% of Millennial buyers say “homeownership is a good investment”. Our problem is that we don’t have enough inventory to pull them out of their apartments and into homes

This is the pent up demand we’ve been waiting to see activate.

Bottom line…its going to be a roller coaster summer.

Thursday, April 10, 2014

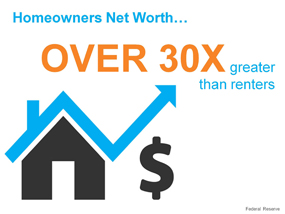

Homeownership’s Impact on Net Worth

Over the last six years, homeownership has lost some of its allure as a financial investment. As homeowners suffered through the housing bust, more and more began to question whether owning a home was truly a good way to build wealth. A study by the Federal Reserve formally answered this question. Over the last six years, homeownership has lost some of its allure as a financial investment. As homeowners suffered through the housing bust, more and more began to question whether owning a home was truly a good way to build wealth. A study by the Federal Reserve formally answered this question.Some of the findings revealed in their report:

Bottom LineThe Fed study found that homeownership is still a great way for a family to build wealth in America. |

Wednesday, April 9, 2014

3 Reasons to Sell Your Home This Spring

Gorgeous weather today! I got some sun yesterday while working in my yard. Spring is almost always a busy time of year in home selling, and this years appears to be no different. Below follows a post by KCM Blog.

3 Reasons to Sell Your Home this Spring

Posted: 08 Apr 2014 04:00 AM PDT

Many sellers are still hesitant about putting their house up for sale. Where are prices headed? Where are interest rates headed? These are all valid questions. However, there are several reasons to sell your home sooner rather than later. Here are three of those reasons.

Many sellers are still hesitant about putting their house up for sale. Where are prices headed? Where are interest rates headed? These are all valid questions. However, there are several reasons to sell your home sooner rather than later. Here are three of those reasons.

Most people realize that the housing market is hottest from April through June. The most serious buyers are well aware of this and, for that reason, come out in early spring in order to beat the heavy competition. We also have a pent-up demand as many buyers pushed off their home search this winter because of extreme weather. Sellers in markets where seasonal weather is never an issue must realize that buyers relocating to their region will increase dramatically this spring as these purchasers finally decide to escape the freezing temperatures of the winters in the north.

These buyers are ready, willing and able to buy…and are in the market right now!

Housing supply always grows from the spring through the early summer. Also, there has been a growing desire for many homeowners to move as they were unable to sell over the last few years because of a negative equity situation. Homeowners have seen a return to positive equity as prices increased over the last eighteen months. Many of these homes will be coming to the market in the near future.

The choices buyers have will continue to increase over the next few months. Don’t wait until all the other potential sellers in your market put their homes up for sale.

If you are moving up to a larger, more expensive home, consider doing it now. Prices are projected to appreciate by approximately 4% this year and 8% by the end of 2015. If you are moving to a higher priced home, it will wind-up costing you more in raw dollars (both in down payment and mortgage payment) if you wait. You can also lock-in your 30 year housing expense with an interest rate at about 4.5% right now. Freddie Mac projects rates to be 5.1% by this time next year and 5.7% by the fourth quarter of 2015.

Moving up to a new home will be less expensive this spring than later this year or next year.

3 Reasons to Sell Your Home this Spring

Posted: 08 Apr 2014 04:00 AM PDT

Many sellers are still hesitant about putting their house up for sale. Where are prices headed? Where are interest rates headed? These are all valid questions. However, there are several reasons to sell your home sooner rather than later. Here are three of those reasons.1. Demand is about to skyrocket

Most people realize that the housing market is hottest from April through June. The most serious buyers are well aware of this and, for that reason, come out in early spring in order to beat the heavy competition. We also have a pent-up demand as many buyers pushed off their home search this winter because of extreme weather. Sellers in markets where seasonal weather is never an issue must realize that buyers relocating to their region will increase dramatically this spring as these purchasers finally decide to escape the freezing temperatures of the winters in the north.

These buyers are ready, willing and able to buy…and are in the market right now!

2. There Is Less Competition - For Now

Housing supply always grows from the spring through the early summer. Also, there has been a growing desire for many homeowners to move as they were unable to sell over the last few years because of a negative equity situation. Homeowners have seen a return to positive equity as prices increased over the last eighteen months. Many of these homes will be coming to the market in the near future.

The choices buyers have will continue to increase over the next few months. Don’t wait until all the other potential sellers in your market put their homes up for sale.

3. There Will Never Be a Better Time to Move-Up

If you are moving up to a larger, more expensive home, consider doing it now. Prices are projected to appreciate by approximately 4% this year and 8% by the end of 2015. If you are moving to a higher priced home, it will wind-up costing you more in raw dollars (both in down payment and mortgage payment) if you wait. You can also lock-in your 30 year housing expense with an interest rate at about 4.5% right now. Freddie Mac projects rates to be 5.1% by this time next year and 5.7% by the fourth quarter of 2015.

Moving up to a new home will be less expensive this spring than later this year or next year.

Monday, April 7, 2014

A Home's Cost vs. Price Explained

I have printed several of these type of illustrations but it is such valuable information so I will print again.

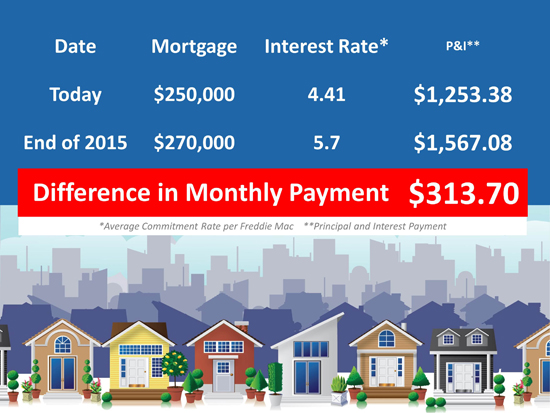

| A Home’s Cost vs. Price Explained Posted: 07 Apr 2014 04:00 AM PDT  We have often talked about the difference between COST and PRICE. As a seller, you will be most concerned about ‘short term price’ – where home values are headed over the next six months. As either a first time or repeat buyer, you must not be concerned about price but instead about the ‘long term cost’ of the home. Let us explain. We have often talked about the difference between COST and PRICE. As a seller, you will be most concerned about ‘short term price’ – where home values are headed over the next six months. As either a first time or repeat buyer, you must not be concerned about price but instead about the ‘long term cost’ of the home. Let us explain.Recently, we reported that a nationwide panel of over one hundred economists, real estate experts and investment & market strategists projected that home values would appreciate by approximately 8% from now to the end of 2015. Additionally, Freddie Mac’s most recent Economic Commentary & Projections Table predicts that the 30 year fixed mortgage rate will be 5.7% by the end of next year. What Does This Mean to a Buyer?Here is a simple demonstration of what impact these projected changes would have on the mortgage payment of a home selling for approximately $250,000 today:  |

Thursday, April 3, 2014

Millennials: Optimistic & Ready to Buy

We believe that 2014 will be the year that Millennials re-enter the housing market in a big way. Because of that, we will be dedicating our blog posts each day this week to a better understanding of this generation. - The KCM Crew

A recent survey by the PulteGroup revealed that the Millennial generation has a more optimistic outlook regarding the American economy than other generations. According to the survey, 54% of Millennials believe the economy is in better shape today than it was last year compared to only 41% of the total population.

A recent survey by the PulteGroup revealed that the Millennial generation has a more optimistic outlook regarding the American economy than other generations. According to the survey, 54% of Millennials believe the economy is in better shape today than it was last year compared to only 41% of the total population.

It seems this optimism is impacting purchasing decisions as 74% of Millennials view now as an excellent or good time to buy the things they want or need. Jim Zeumer, vice president of corporate communications for the PulteGroup explained:

"No other cohort of adults is nearly as confident about their economic future as the millennials are right now. This is definitely a change, as millennials have regularly been viewed as the disenfranchised generation vastly affected by the fallout of the recession. But now, with an increased sense of optimism, this generation is starting to feel as though they have the resources available to lead the lives they want or expect to in the future."

Specific to real estate, the survey indicated:

A recent survey by the PulteGroup revealed that the Millennial generation has a more optimistic outlook regarding the American economy than other generations. According to the survey, 54% of Millennials believe the economy is in better shape today than it was last year compared to only 41% of the total population.It seems this optimism is impacting purchasing decisions as 74% of Millennials view now as an excellent or good time to buy the things they want or need. Jim Zeumer, vice president of corporate communications for the PulteGroup explained:

"No other cohort of adults is nearly as confident about their economic future as the millennials are right now. This is definitely a change, as millennials have regularly been viewed as the disenfranchised generation vastly affected by the fallout of the recession. But now, with an increased sense of optimism, this generation is starting to feel as though they have the resources available to lead the lives they want or expect to in the future."

WHAT ABOUT HOUSING?

Specific to real estate, the survey indicated:

- 85% of Millennials plan to purchase a home in the future

- 49% plan to purchase a home in the next two years

- Of those planning to purchase in the near-term, 56 percent are current homeowners and 41 percent are renters

- 65% prefer spending more money on a home that is move-in ready compared to doing renovations

- 58% increased their interest in purchasing a home in the past year as the positive attributes of homeownership resonate with this generation.

Wednesday, April 2, 2014

National Trends

The year got off to a cool start as cold and snowfall slowed sales in the East and Midwest and continuing tight credit conditions along with weak inventories kept sales underperforming throughout the country. In coastal areas, flood insurance uncertainties remain a factor. Trend lines are from January 2013 to January 2014.

Tuesday, April 1, 2014

Interest Rates

DID YOU KNOW?... Since Freddie Mac began tracking mortgage rates in 1971, the all-time high was hit in October 1981, at 18.63%. That's more than 4 times recent average 30-year fixed mortgage rates.

The PTC Report for February

February 2014

| Building Permits | 258 |

| New Home Sales | 126 |

| Existing Home Sales | 474 |

| Refinance | 630 |

| Average Sales Price | 185159.5 |

| Financial-Bond Market(10-yr Treasury) | 2.71 |

| Days on Market | 67.5 |

| Distressed(Short Sales and REO) | 1147 |

| Notices of Default | 161 |

| PTC Index | 132 |

The last full month of the winter season is behind us; February showed some positive numbers heading into the Spring. Building Permits inched up just slightly in January, but jumped by 18 percent in February. In the year ago time period, building permits stayed consistent at just a light increase of 2.4 percent. New home sales stayed flat from a year ago, but fell slightly by 5.3 percent from the month prior while existing home sales inched up slightly by just over 1 percent in the same period. After a long period of sharp monthly declines, refinances seem to be leveling out - down just 7.2 percent from the month prior (down roughly 60 percent from February 2013). After a long stint of systematic increases, the average Treasure Valley sales price dropped slightly by 5 percent, but still up 11.4 percent form a year which may be an indication of stabilization in home values. Notices of default continue to fall, while distressed properties (short sales and REO) rose slightly by 5 percent which will be an area to watch in the coming weeks.

Subscribe to:

Posts (Atom)