by Marc Lebowitz, RCE, CAE

Executive Director, Ada County Association of REALTORS

Single family home sales in December 2013 were 569 in Ada County, an increase of 12% compared to December 2012. December sales were surprisingly strong; erasing two months of lackluster numbers and contributing to a strong 2013.

Year-to-date sales are 7,957; up 14% over 2012 YTD sales of 6,979.

Dollar volume for December was up 26% to $136 million and YTD we are just over $1.8 billion in sales.

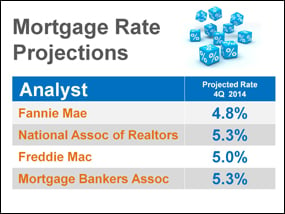

The fourth quarter of 2013 brought worry (over what would happen to mortgage rates in 2014), frustration (over the Government shutdown and how that severely impacted our ability to close business in October) and uncertainty about the continuation of tax forgiveness for sellers in short sale deals.

In the end, the juggernaut that was 2013 overpowered all of those negatives and finished strong.

Days on market averaged 59 in December, up nearly a week from November. Our year-to-date average is 52 days.

New homes sold in December totaled 134; up 16% from December 2012.

Historically, December sales decline from November by an average of 2%. December 2013 posted a 4% increase over November 2013.

Of the total sales in December, 11% were distressed; up 1% from last month. In December 2012, 24% of sales were distressed.

For the month of December, REO sales (55% of Distressed; 34 total sales) exceeded Short Sales (45% of Distressed; 28 total sales), for the second consecutive month.

Pending sales at the end of December were 686; down 13% from December 2012.

Of Pending sales in distress (15%), there was a decrease in the number of Short Sales (from 59% to 57% of activity; 58 total sales) and a increase in REO sales (from 41% to 43%; 44 total sales).

December median home price was $198,512; up 11% from December 2012. Our 2013 YTD median home price is $198,000; up 16% for the year.

New Homes median price for December was $280,500; up 19% from December 2012. For Existing homes the increase is 13% to $183,000.

The number of houses available for sale at the end of December decreased 10% from November 2013 to 2,016. This is the fourth consecutive month of decrease. This is 15% more than last year at this time. Since January we have increased the number of single family homes for sale by 21%, allowing us to grow our YTD sales increase.

Historically, inventory decreases steadily from August to December.

Of the total active listings, 12% are distressed, up 1% from the end of November 2013.

With inventory experiencing seasonal decreases and the percentage of distressed inventory holding very low, median home price will remain strong through the end of this year.

Of our Distressed Inventory, 69% is Short Sales (166) and 31% is REO (74).

Available inventory decreased at all price points.

In Ada County we now have 3.6 months of inventory on hand, up a little from the end of November.

The price category in shortest supply is <$100K where we have 1.6 months.

From $100,000 to $160,000 we have less than 3 months available inventory.

From $160,000 to $300,000 we have slightly less than 4 months.

Above $300,000 we have a 4+ month’s supply. Above $500,000 the supply is closer to five months. Remembering that six months of available inventory describes a “stable real estate market”; it looks like we are heading into a period of “normal” like we haven’t seen in several years.

Of sales in December, the most popular price point was $160,000 to $200,000 (23%); followed by $120,000 to $160,000 (20%), $200,000 to $250,000 with 14%.

So…what’s next?

Lawrence Yun, NAR chief economist, said the market is being squeezed. “Home sales are hurt by higher mortgage interest rates, constrained inventory and continuing tight credit,” he said. “There is a pent-up demand for both rental and owner-occupied housing as household formation will inevitably burst out, but the bottleneck is in limited housing supply, due to the slow recovery in new home construction. As such, rents are rising at the fastest pace in five years, while annual home prices are rising at the highest rate in eight years.”

For Ada County, the positives that have helped push the pace of our recovery past the national average are still in place; growing population, jobs creation and quality of life issues will bridge us through the slow winter months.

Growing up it seemed ‘white lies’ were okay while lying was a sin. As children, we sometimes had difficulty understanding where the line was. As we matured, we realized there most definitely was a difference.

Growing up it seemed ‘white lies’ were okay while lying was a sin. As children, we sometimes had difficulty understanding where the line was. As we matured, we realized there most definitely was a difference. If you are thinking about purchasing a home right now, you are surely getting a lot of advice. Though your friends and family have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Let’s look at whether or not now is actually a good time for you to buy a home.

If you are thinking about purchasing a home right now, you are surely getting a lot of advice. Though your friends and family have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Let’s look at whether or not now is actually a good time for you to buy a home.

The price of any item (including residential real estate) is determined by ‘supply and demand’. If many people are looking to buy an item and the supply of that item is limited, the price of that item increases.

The price of any item (including residential real estate) is determined by ‘supply and demand’. If many people are looking to buy an item and the supply of that item is limited, the price of that item increases.