Today we are excited to have Nabil Captan as our guest blogger. Nabil is a nationally recognized credit scoring expert, educator, author and producer. In today’s post, he explains how what you don’t know about your credit score could end up costing you. Enjoy! – The KCM Crew

Today we are excited to have Nabil Captan as our guest blogger. Nabil is a nationally recognized credit scoring expert, educator, author and producer. In today’s post, he explains how what you don’t know about your credit score could end up costing you. Enjoy! – The KCM Crew Informed consumers considering a home purchase today want to do the right thing and plan ahead. Many do not seek immediate professional guidance from a Realtor or a mortgage loan officer. Instead, they hunt for hours online, looking at numerous websites for available homes for sale. They also consult websites to find the best interest rate and terms for future monthly mortgage payments. Many consumers feel betrayed, cheated and at times embarrassed to learn that the credit scores they counted on, to get that specific interest rate for their loan, are not used by mortgage lenders. When shopping for a good mortgage interest rate, consumers also need to know their credit score, and utilize an online mortgage calculator to compute future monthly mortgage payments. A Google search for “credit score” will yield hundreds of results. The consumer accepts the provider’s terms and conditions to get a

free credit score. Terrific! Unaware that in exchange they just received a meaningless credit score that lenders

never use. They also handed over their Non-Public Personal Information (NPPI) to that credit score provider for

life. Before we go any further, let’s look at available credit scoring products available to consumers today:

- FICO credit score from Fair Isaac Corporation/myfico.com, range 300 to 850

- Plus Score from Experian, range 320 to 830

- Trans Risk Score from TransUnion, range 300 to 850

- Equifax Credit Score from Equifax, range 300 to 850

- Vantage Score from all three bureaus, two ranges, 300 to 850 and 501-990

What is a FICO Score?

In 1958, Bill Fair and Earl Isaac, a mathematician and engineer, formed a company in San Rafael, California. They created tools to help risk managers make a better decision when taking financial risk. Today, 90 percent of all lenders use the

FICO score, first created in 1989 by Fair Isaac, and it’s the

only score Fannie Mae and Freddie Mac, the Federal Housing Agency and Veterans Affairs will accept in underwriting loans they guarantee.

What is a Consumer Score?

The three credit bureaus, in their understanding of the credit scoring model created by FICO, decided to create their own scoring models, and in 2004 – 2006 they unveiled the “consumer” scores:

Plus Score,

Trans Risk Score,

Equifax Credit Score, and

Vantage Score. However, these are not genuine FICO scores, and mortgage lenders don’t use them. Consider this comparison:

Would you buy a watch that gives the approximate time of day? The three credit bureaus work with major financial institutions, professional organizations, comparison sites, personal finance businesses, clubs such as Costco, AAA, Sam’s Club, and many data-mining brokers to bombard consumers in the race of the

free credit score mania, all with the enticement of a “consumer” score that is not used by lenders, in hopes of obtaining subscriptions or fees from consumers. Fees that are totally unnecessary!

Know Your Score

Gaining access to one’s own credit report and credit score prior to loan approval with no strings attached could be helpful, and at all times beneficial. With little effort, inaccuracy of information can be instantly corrected at the credit bureau level, and with a few simple steps, credit scores could be enhanced. For example, paying down revolving account balances before a creditor’s statement-ending date (the creditor later updates account information with the credit bureaus), thus reducing revolving account balances at a particular point in time, will positively add more points to a score. It’s priceless.

More Information

Consumers have a legal right to access their annual credit report at no charge once a year from

annualcreditreport.com, a site sponsored by the three major credit bureaus: Experian, Equifax and TransUnion. These reports provide all the basic consumer data, but do not reveal a credit score. If you have a need for the FICO credit score that is actually used by mortgage lenders,

myfico.com is the website to visit. For $19.95 per bureau, consumers can purchase a customized credit report with a genuine FICO score. Additional websites to visit: the Federal Trade Commission (

ftc.gov) and the Consumer Financial Protection Bureau (

cfpb.gov) for true answers to questions about any financial concepts, financial products, dispute and complaint submissions, and much more.

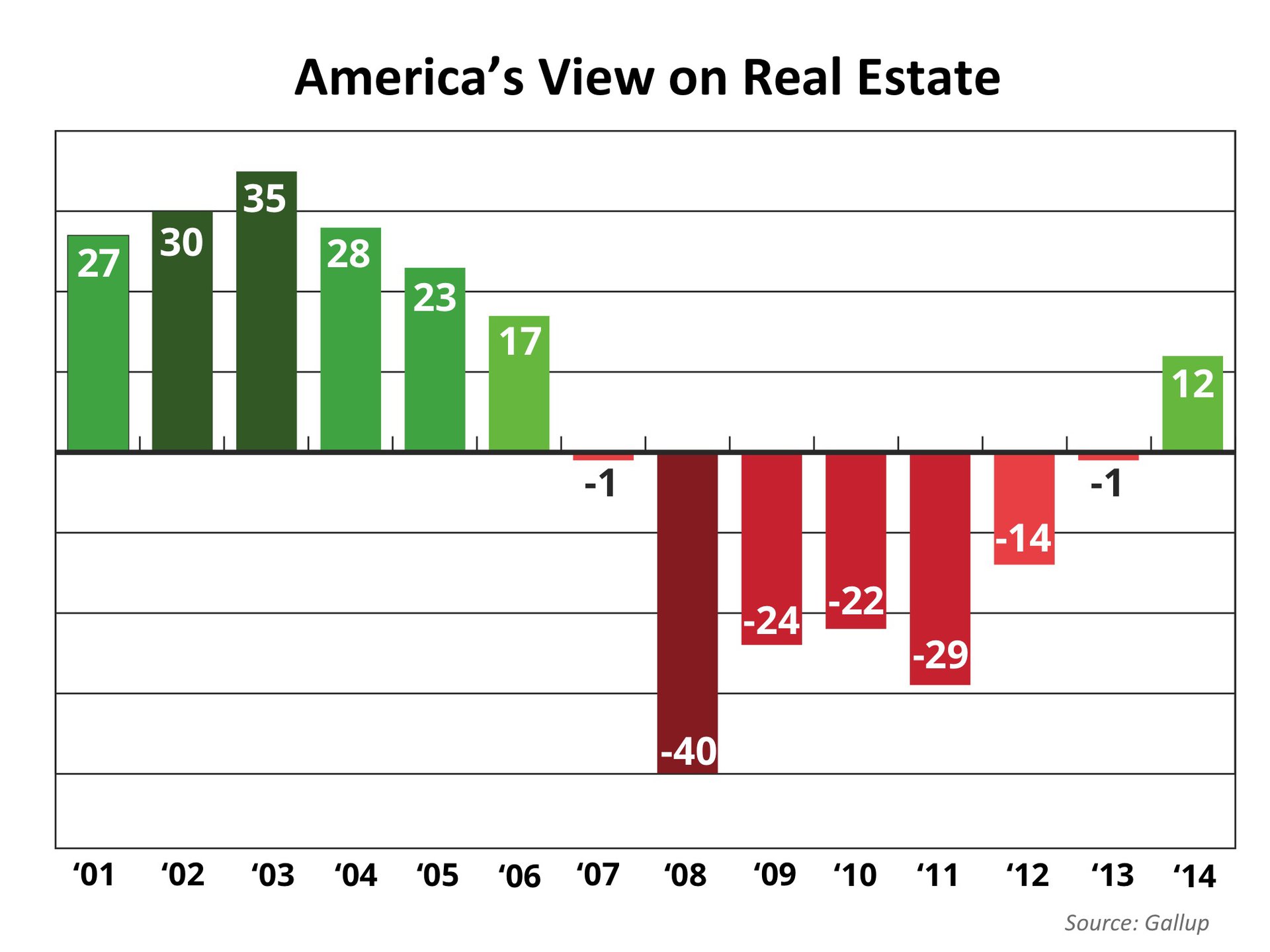

It seems that an improving economy and jobs market will mean a very healthy housing market.

It seems that an improving economy and jobs market will mean a very healthy housing market.

The New York Times recently published an editorial entitled, “

The New York Times recently published an editorial entitled, “

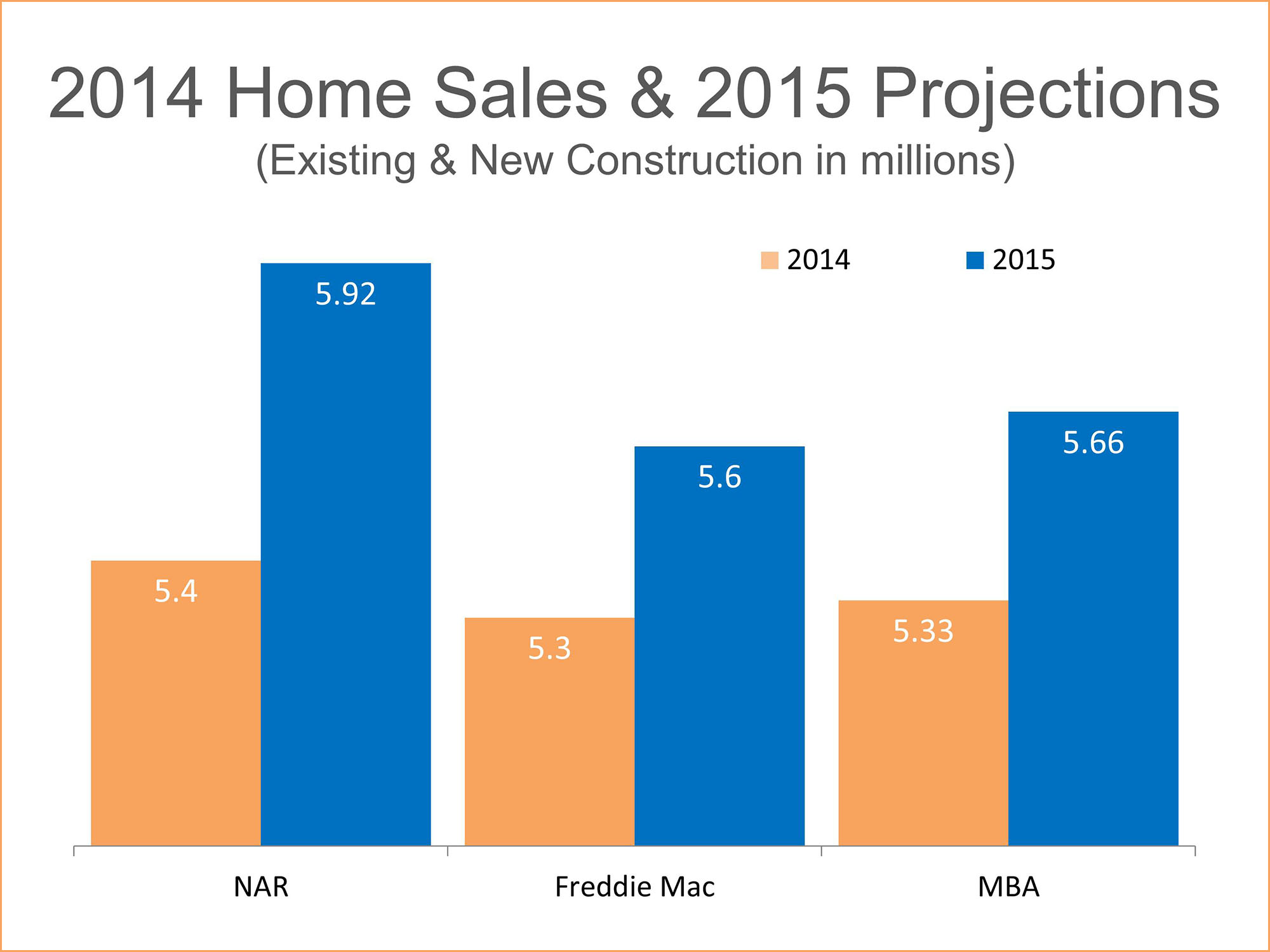

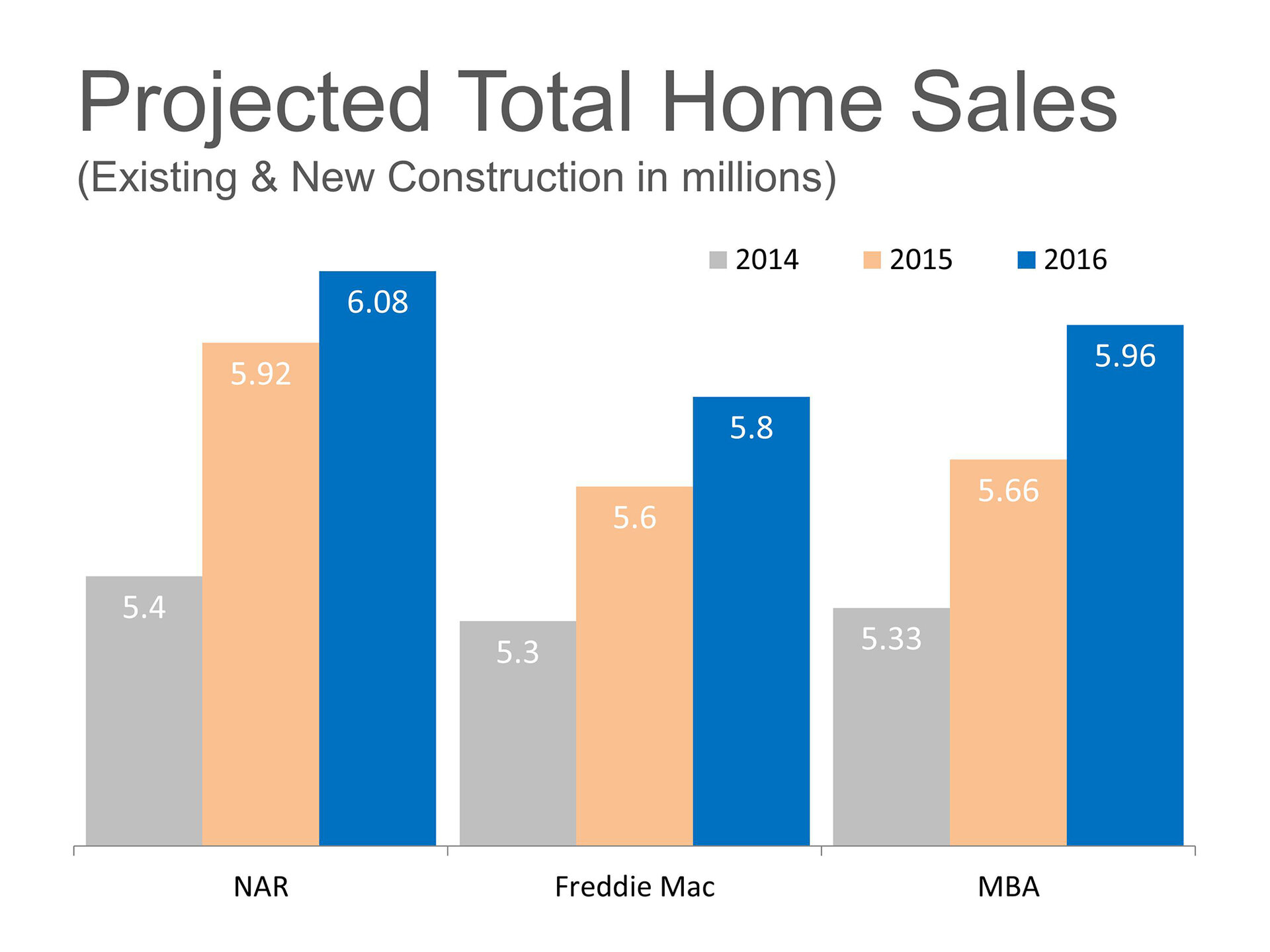

As we finish 2014, it appears the real estate market is once again on solid footing and ready to advance forward over the next few years. The strength of the market can be viewed using two metrics: projected home values and projected house sales. We recently reported that the Home Price Expectation Survey revealed future home values will continue to appreciate nicely. Today we want to look at projections on the number of home sales (existing and new construction) we will see over the next two years. We researched what the National Association of Realtors (NAR), Freddie Mac and the Mortgage Bankers’ Association(MBA) are projecting for the housing industry going forward. Here is what we found:

As we finish 2014, it appears the real estate market is once again on solid footing and ready to advance forward over the next few years. The strength of the market can be viewed using two metrics: projected home values and projected house sales. We recently reported that the Home Price Expectation Survey revealed future home values will continue to appreciate nicely. Today we want to look at projections on the number of home sales (existing and new construction) we will see over the next two years. We researched what the National Association of Realtors (NAR), Freddie Mac and the Mortgage Bankers’ Association(MBA) are projecting for the housing industry going forward. Here is what we found:

Eric Belsky is Managing Director of the Joint Center of Housing Studies at Harvard University. He also currently serves on the editorial board of the Journal of Housing Research and Housing Policy Debate. Last year, he released a paper on homeownership -

Eric Belsky is Managing Director of the Joint Center of Housing Studies at Harvard University. He also currently serves on the editorial board of the Journal of Housing Research and Housing Policy Debate. Last year, he released a paper on homeownership -

A

A  If you are thinking about purchasing a home right now, you are surely getting a lot of advice. Though your friends and family have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Let’s look at whether or not now is actually a good time for you to buy a home. There are three questions you should ask before purchasing in today’s market:

If you are thinking about purchasing a home right now, you are surely getting a lot of advice. Though your friends and family have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Let’s look at whether or not now is actually a good time for you to buy a home. There are three questions you should ask before purchasing in today’s market:

The National Association of Realtors (NAR) released their

The National Association of Realtors (NAR) released their

Billionaire money manager John Paulson was

Billionaire money manager John Paulson was

For the last several years, home sellers had to compete with huge inventories of distressed properties (foreclosures and short sales). The great news is that the supply of these properties is falling like a rock in the vast majority of housing markets (only

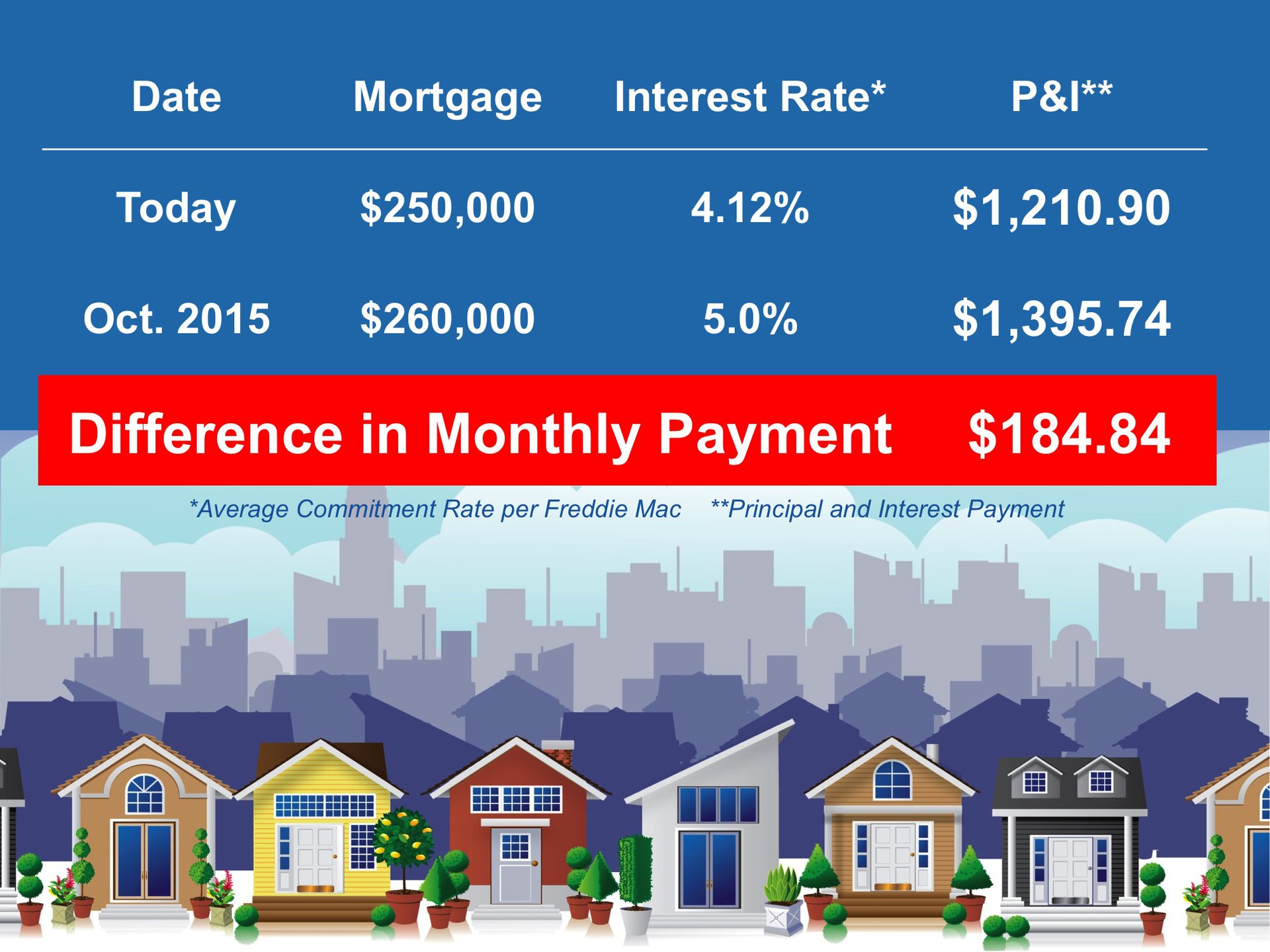

For the last several years, home sellers had to compete with huge inventories of distressed properties (foreclosures and short sales). The great news is that the supply of these properties is falling like a rock in the vast majority of housing markets (only  We have often talked about the difference between COST and PRICE. As a seller, you will be most concerned about ‘short term price’ – where home values are headed over the next six months. As either a first time or repeat buyer, you must not be concerned about price but instead about the ‘long term cost’ of the home.

We have often talked about the difference between COST and PRICE. As a seller, you will be most concerned about ‘short term price’ – where home values are headed over the next six months. As either a first time or repeat buyer, you must not be concerned about price but instead about the ‘long term cost’ of the home.

A recent

A recent

In a

In a

In a recent survey,

In a recent survey,  The National Association of Realtors (NAR) compiled data from research conducted by the Bureau of Economic Analysis & Macroeconomic Advisors on the economic impact of a home purchase. After reviewing the

The National Association of Realtors (NAR) compiled data from research conducted by the Bureau of Economic Analysis & Macroeconomic Advisors on the economic impact of a home purchase. After reviewing the  In Trulia’s 2014

In Trulia’s 2014

The safest drivers in America, for the fourth year in a row, hail from

The safest drivers in America, for the fourth year in a row, hail from  Drivers in the city of 150,000 north of Denver can expect to go 14.2 years between accidents, according to the insurance giant’s claims data. Contrast that with 200th-ranked Worcester, Massachusetts, where drivers go just 4.3 years between claims.

Drivers in the city of 150,000 north of Denver can expect to go 14.2 years between accidents, according to the insurance giant’s claims data. Contrast that with 200th-ranked Worcester, Massachusetts, where drivers go just 4.3 years between claims.