Recently, HousingWire asked David Berson, chief economist at Nationwide, for his opinion on the near-term future of housing. Below are what Mr. Berson believes to be the three things you need to know about housing in 2014. We have included a quote from the article and a small comment from KCM for all three points.

Recently, HousingWire asked David Berson, chief economist at Nationwide, for his opinion on the near-term future of housing. Below are what Mr. Berson believes to be the three things you need to know about housing in 2014. We have included a quote from the article and a small comment from KCM for all three points.Number 1: 2014 should prove to be the strongest year for housing activity since before the Great Recession

“Most economists expect an improved job market in 2014, with employment growth accelerating and the unemployment rate continuing to decline. That jobless rate drop will reflect more of a pickup in employment than further declines in the labor force participation rate. This will be the key factor improving housing demand this year, even if mortgage rates rise and affordability declines. While the housing market tends to do especially well when the job market improves and mortgage rates decline simultaneously, that combination of events occurs only rarely…People buy homes when their job and income prospects improve – even if it’s more expensive to do so – rather than buy when it is inexpensive to do so but they’re worried about keeping their jobs.”

KCM Comment:

We agree that the job market will continue to improve and that rising interest rates will not be a detriment to the market in 2014. As Doug Duncan, SVP and chief economist at Fannie Mae, recently revealed:

“Consumers have taken the interest rate rise in stride. Expectations for continued improvement in housing persist, and sentiment toward the current buying and selling environment is back on track.”

Number 2: Demographics should start to favor housing activity

“If the economy expands at a faster pace this year, bringing a more rapid rate of job creation, that should translate into more households, raising housing demand. We won’t see all three million missing households return to the housing market at once. (That wouldn’t be a good thing for the housing market anyway, since that would be on top of the 1.2 million households that normally would develop this year; such a surge would swamp the existing housing supply). Beginning in 2014, the pace of household formations should accelerate to an above-trend pace for several years, pushing up housing demand.”

KCM Comment:

The Urban Land Institute recently released a report, Emerging Trends in Real Estate 2014, projecting that 4.48 million new households will be formed over the next three years. Millennials will make up a large portion of these new households. With the economy improving, we believe they will finally be moving out of their parents’ homes and, after they compare renting versus buying, many will choose homeownership.

Number 3: Mortgage availability shouldn’t worsen and may improve

“The rise in mortgage rates already has reduced mortgage origination volumes as refinance activity declines. If mortgage rates rise further this year, as expected, then refinance activity will fall still more. In response, mortgage lenders probably will ease lending standards to the extent possible under the QM rules to boost lending activity by increasing purchase originations. As a result, the increase in new households expected to be created this year, spurred by a stronger job market, should find that qualifying for a mortgage loan will be somewhat easier in 2014 than in prior years.”

KCM Comment:

We also believe that, as the refinancing market begins to dry up, mortgage entities will be more aggressive in the purchase money market (mortgages necessary to purchase a home). There even seems to be recent evidence that lending standards are actually loosening.

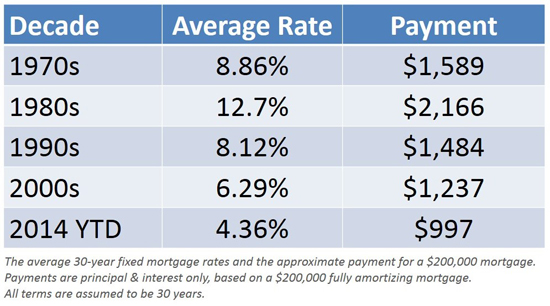

"One thing seems certain: we aren't likely to see average 30-year fixed mortgage rates return to the historic lows experienced in 2012."

"One thing seems certain: we aren't likely to see average 30-year fixed mortgage rates return to the historic lows experienced in 2012."

Many sellers are still hesitant about putting their house up for sale. Where are prices headed? Where are interest rates headed? Can buyers qualify for a mortgage? These are all valid questions. However, there are several reasons to sell your home sooner rather than later. Here are five of those reasons.

Many sellers are still hesitant about putting their house up for sale. Where are prices headed? Where are interest rates headed? Can buyers qualify for a mortgage? These are all valid questions. However, there are several reasons to sell your home sooner rather than later. Here are five of those reasons. Based on prices, mortgage rates and soaring rents, there may have never been a better time in real estate history to purchase a home than right now. Here are five major reasons purchasers should consider buying.

Based on prices, mortgage rates and soaring rents, there may have never been a better time in real estate history to purchase a home than right now. Here are five major reasons purchasers should consider buying.

Location may have the most effect on value but Price is without question the most important factor controlling the sale of real estate. Anything will sell anytime, how long will it take depends on the price.

Location may have the most effect on value but Price is without question the most important factor controlling the sale of real estate. Anything will sell anytime, how long will it take depends on the price. You may be frustrated while attempting to buy a home in today’s market. You may feel powerless to the process. How could YOU possibly know whether the current good news about housing will continue? There is no doubt that today’s real estate market is extremely difficult to navigate. However, we want you to know that thousands of homes sold yesterday, thousands will sell today and thousands will sell each and every day from now until the end of the year.

You may be frustrated while attempting to buy a home in today’s market. You may feel powerless to the process. How could YOU possibly know whether the current good news about housing will continue? There is no doubt that today’s real estate market is extremely difficult to navigate. However, we want you to know that thousands of homes sold yesterday, thousands will sell today and thousands will sell each and every day from now until the end of the year.