Monday, September 29, 2014

Saturday, September 27, 2014

Rudest Drivers Are in IDAHO?

I normally like to do positive posts, especially on the non-real estate topics. but I found this article interesting.

From Boise Weekly:

For all of the polls and surveys that tell Idahoans how wonderfully liveable our state is, a new study out this morning is a swift kick in the butt for the Gem State.

Insure.com insists that Idaho has the rudest drivers in the nation.

A survey of 2,000 drivers nationwide asked drivers to name those they think are the rudest in other states.

And Idaho came out the worst. This morning's USA Today writes, "They honk, they're impatient, they make rude gestures, they gun their engines. They are the rude drivers, and the highest concentration of them is in Idaho, a new poll suggests."

Idaho was followed by Washington, D.C., New York, Wyoming, Massachusetts, Delaware, Vermont, New Jersey, Nevada and Utah.

Here's the the write-up from Insure.com:

From Boise Weekly:

For all of the polls and surveys that tell Idahoans how wonderfully liveable our state is, a new study out this morning is a swift kick in the butt for the Gem State.

Insure.com insists that Idaho has the rudest drivers in the nation.

A survey of 2,000 drivers nationwide asked drivers to name those they think are the rudest in other states.

And Idaho came out the worst. This morning's USA Today writes, "They honk, they're impatient, they make rude gestures, they gun their engines. They are the rude drivers, and the highest concentration of them is in Idaho, a new poll suggests."

Idaho was followed by Washington, D.C., New York, Wyoming, Massachusetts, Delaware, Vermont, New Jersey, Nevada and Utah.

Here's the the write-up from Insure.com:

1. Idaho: Wait for it

The roadways of Idaho present a dichotomy of drivers: Those who are moving so slowly that they’re judged to be rude, and the aggressive drivers who speed around them and flip them off. Together, with their opposite yet equally vexing styles of driving, they push Idaho to the top of the rankings.

Remember Matt Stubbs, formerly of Utah? He recently moved to Idaho and was amazed by the number of drivers holding up everyone behind them, moving at turtle-like speed, reminiscent of an old-fashioned Sunday drive.

“Maybe I’m just used to the aggressive, overly-caffeinated (on Diet Coke) Utah drivers. That’s why everyone in Idaho seems to be driving so slowly,” he says.

Stubbs observes that Idahoans feel “just fine taking their time, driving 5 to 10 miles an hour under the limit.”

This creates additional tension when fast drivers are added to the mix. Idaho resident Eric Leins, a Southern California native, points to the state’s mountainous, rural areas as a source of driver conflict. Those familiar with certain roads may not be very patient with drivers new to the twisting, turning roadways.

“If you’ve driven that hundreds of times, you know [the road] and pick up your speed,” he says. “So those driving them for the first time may have the experienced drivers honking their horns and flipping them the bird,” he says.

Despite its No. 1 ranking for rude driving, Idaho insurance premiums are among the lowest in the nation. Idaho premiums rank No. 48 out of 51 in Insure.com's 2014 study of car insurance rates by state.

Friday, September 26, 2014

Gallup Poll: Real Estate “Heading in the Right Direction”

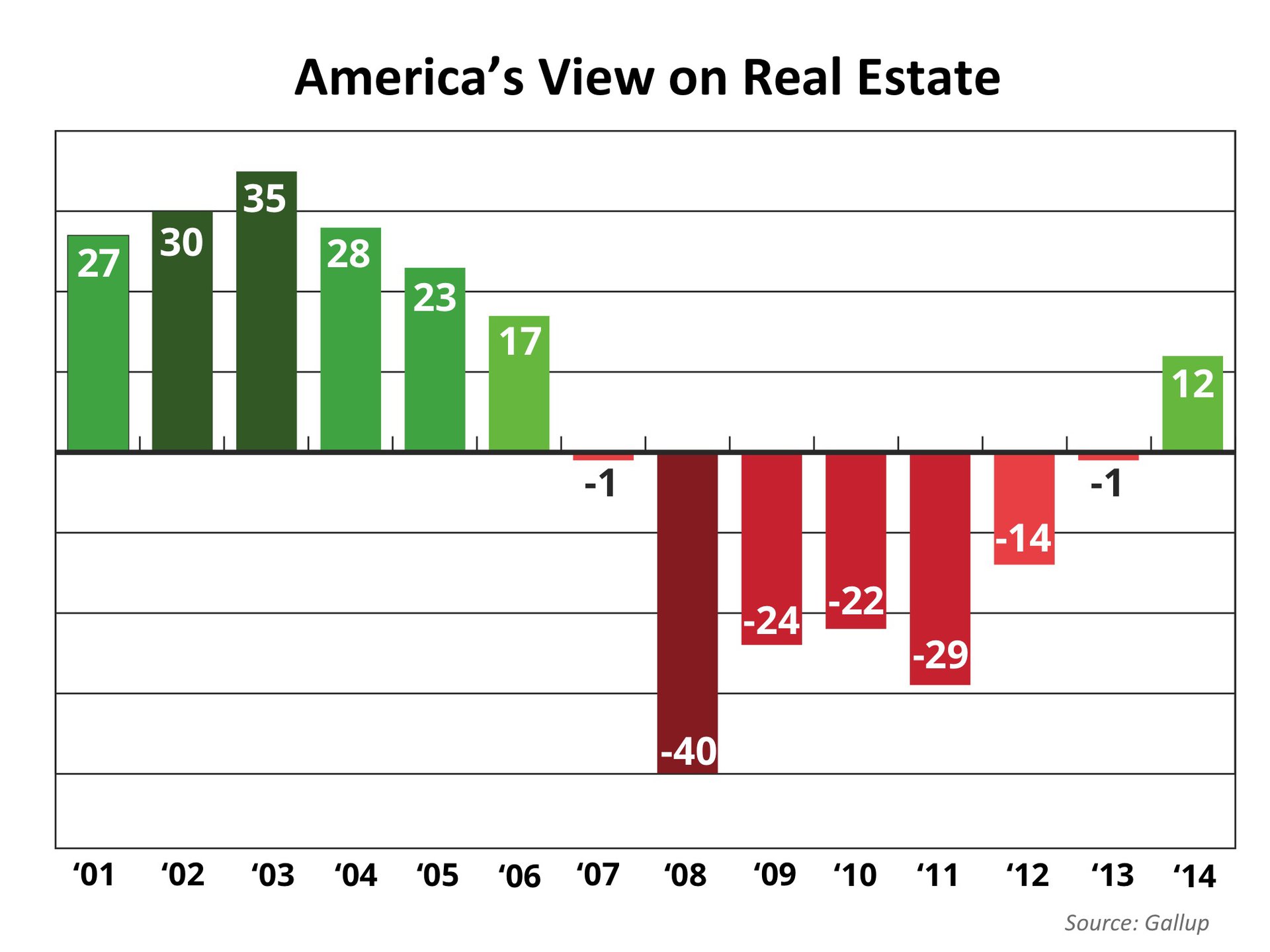

In a recent Gallup poll, Americans were asked to rate 24 different business sectors and industries on a five-point scale ranging from "very positive" to "very negative." The poll was first conducted in 2001, and has been used as an indicator of “Americans’ overall attitudes toward each industry”. For the first time since 2006, Americans had an overall positive view of real estate, giving the industry a 12% positive ranking.

In a recent Gallup poll, Americans were asked to rate 24 different business sectors and industries on a five-point scale ranging from "very positive" to "very negative." The poll was first conducted in 2001, and has been used as an indicator of “Americans’ overall attitudes toward each industry”. For the first time since 2006, Americans had an overall positive view of real estate, giving the industry a 12% positive ranking. Americans’ view of the real estate industry worsened from 2003 to the -40% plummet of 2008. Gallup offers some insight into the reason for decline:

Americans’ view of the real estate industry worsened from 2003 to the -40% plummet of 2008. Gallup offers some insight into the reason for decline:Prices Dropped

“In late 2006, real estate prices in the U.S. began falling rapidly, and continued to drop. Many homeowners saw their home values plummet, likely contributing to real estate's image taking a hard hit.”

Housing Bubble

“The large drops in the positive images of banking and real estate in 2008 and 2009 reflect both industries' close ties to the recession, which was precipitated in large part because of the mortgage-related housing bubble.”

Bottom Line

“Although the image of real estate remains below the average of 24 industries Gallup has tracked, the sharp recovery from previous extreme low points suggests it is heading in the right direction.”

Thursday, September 25, 2014

The Truth About Buying a Home: You DON'T Need 20% Down

Answering some apparently common mis-conceptions about buying a home.

In a recent survey, How America Views Homeownership, it was revealed that 68% of Americans feel that now is a good time to buy a home and 95%said they want to own a home if they don’t already. Franklin Codel, head of Wells Fargo home mortgageproduction, explains:

In a recent survey, How America Views Homeownership, it was revealed that 68% of Americans feel that now is a good time to buy a home and 95%said they want to own a home if they don’t already. Franklin Codel, head of Wells Fargo home mortgageproduction, explains:

However, the survey also reported that many are afraid to purchase a home because of uncertainty about “qualifying for a mortgage or navigating the home buying process”. Though 74% said they “know and understand” the financial process involved in buying a home, they also gave answers that suggest otherwise. For example:

In actuality many of these beliefs are unfounded. Let’s look at the question of down payment: Freddie Mac, in a recent blog post addressing the issue, confirmed that there is misinformation regarding the amount necessary when determining the down payment for a home purchase:

In a separate Executive Perspectives, Christina Boyle, Freddie Mac’s VP and Head of Single-Family Sales & Relationship Management explained further:

Boyle talked about the importance of educating potential buyers:

Codel agreed:

If you are saving for either your first home or that perfect move-up dream house, make sure you know all your options. You may be pleasantly surprised. ___________________________________________________________________

In a recent survey, How America Views Homeownership, it was revealed that 68% of Americans feel that now is a good time to buy a home and 95%said they want to own a home if they don’t already. Franklin Codel, head of Wells Fargo home mortgageproduction, explains:“Although the home buying process has changed in many ways in recent years, our survey found Americans still view homeownership as an achievement to be proud of and many believe that now is a good time to buy a home.”

Confusion Creates Paralysis

However, the survey also reported that many are afraid to purchase a home because of uncertainty about “qualifying for a mortgage or navigating the home buying process”. Though 74% said they “know and understand” the financial process involved in buying a home, they also gave answers that suggest otherwise. For example:

- 30% of respondents believe that only individuals with high incomes can obtain a mortgage

- 64% of respondents believe they must have a “very good” credit score to buy a home

- 44% believe that a 20% down payment is required

In actuality many of these beliefs are unfounded. Let’s look at the question of down payment: Freddie Mac, in a recent blog post addressing the issue, confirmed that there is misinformation regarding the amount necessary when determining the down payment for a home purchase:

“Did you know 40 percent of today's homebuyers using mortgage financing are making down payments that are less than 10 percent? And how about this: since 2010, the number of people putting down less than 10 percent for conventional loans has grown three fold. So, not only are low down payment options real, they represent a significant portion of today's purchases.”

In a separate Executive Perspectives, Christina Boyle, Freddie Mac’s VP and Head of Single-Family Sales & Relationship Management explained further:

- A person “can get a conforming, conventional mortgage with a down payment of as little as 5 percent (sometimes with as little as 3 percent coming out of their own pockets)”.

- Qualified borrowers can further reduce the down payment coming out of their own pockets to 3 percent by lining up gifts from family, grants or loans from non-profits or public agencies.

Education is the Key

Boyle talked about the importance of educating potential buyers:

“Letting more consumers know how down payments are determined could bring more qualified borrowers off the sidelines. Depending on their credit history and other factors, many borrowers can expect to make a down payment of about 5 or 10 percent.”

Codel agreed:

“It is important for prospective homebuyers to feel empowered to ask lenders and real estate agents questions about available options, such as down payment assistance or FHA loan programs or VA loans for veterans.”

Bottom Line

If you are saving for either your first home or that perfect move-up dream house, make sure you know all your options. You may be pleasantly surprised. ___________________________________________________________________

Monday, September 22, 2014

Home Sales Generate $52,205 Impact on Economy

The National Association of Realtors (NAR) compiled data from research conducted by the Bureau of Economic Analysis & Macroeconomic Advisors on the economic impact of a home purchase. After reviewing the data, they concluded that the total economic impact of a typical home sale in the United States is an astonishing $52,205.Here is the breakdown of their report:

The National Association of Realtors (NAR) compiled data from research conducted by the Bureau of Economic Analysis & Macroeconomic Advisors on the economic impact of a home purchase. After reviewing the data, they concluded that the total economic impact of a typical home sale in the United States is an astonishing $52,205.Here is the breakdown of their report: Economic Contributions are derived from:

- Home construction

- Real estate brokerage

- Mortgage lending

- Title insurance

- Rental and Leasing

- Home appraisal

- Moving truck service

- Other related activities

When a House is Sold in the United States:

$15,912 of income is generated from real estate related industries. New homeowners spend an additional $4,429 on consumer items such as furniture, appliances, and remodeling. It generates an economic multiplier impact. There is a greater sense of community associated with owning a home; therefore there is greater spending at restaurants, sports games, and charity events. The size of this “multiplier” effect is estimated to be: $9,764 Additional home sales induce additional home production. Typically one new home is constructed for every 8 existing home sales. Therefore, for each existing home sale, 1/8 of new home value is added to the economy, which is estimated in the U.S. to be: $22,100

When you add the numbers up it comes to $52,205!

Tuesday, September 16, 2014

Thursday, September 11, 2014

Buying a Home is 38% Less Expensive than Renting!

In Trulia’s 2014 Rent vs. Buy Report, they explained that homeownership remains cheaper than renting throughout the 100 largest metro areas in the United States; ranging from an average of 5% in Honolulu, all the way to 66% in Detroit, and 38% Nationwide! The other interesting findings in the report include:

In Trulia’s 2014 Rent vs. Buy Report, they explained that homeownership remains cheaper than renting throughout the 100 largest metro areas in the United States; ranging from an average of 5% in Honolulu, all the way to 66% in Detroit, and 38% Nationwide! The other interesting findings in the report include:Even though prices increased sharply in many markets over the past year, low mortgage rates have kept homeownership from becoming more expensive than renting.

Some markets might tip in favor of renting later this year as prices continue to rise faster than rents and if – as most economists expect – mortgage rates rise, due both to the strengthening economy and Fed tapering.

Nationally, rates would have to rise to 10.6% for renting to be cheaper than buying – and rates haven’t been that high since 1989.

Bottom Line

Buying a home makes sense. Rental costs have historically increased at a higher rate of inflation. Lock in a mortgage payment now before home prices and mortgage rates rise as experts expect they will.

Tuesday, September 9, 2014

Winter is coming! Should you Buy NOW?

It's that time of year, the seasons are changing and with them bring thoughts of the upcoming holidays, family get togethers, and planning for a new year. Those who are on the fence about whether now is the right time to buy don't have to look much farther to find four great reasons to consider buying a home now, instead of waiting.

1. Prices Will Continue to Rise

The Home Price Expectation Survey polls a distinguished panel of over 100 economists, investment strategists, and housing market analysts. Their most recent report released recently projects appreciation in home values over the next five years to be between 11.2% (most pessimistic) and 27.8% (most optimistic).

The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

2. Mortgage Interest Rates Are Projected to Increase

Although Freddie Mac’s Primary Mortgage Market Survey shows that interest rates for a 30-year mortgage have softened recently, most experts predict that they will begin to rise later this year. The Mortgage Bankers Association, Fannie Mae, Freddie Mac and the National Association of Realtors are in unison projecting that rates will be up almost a full percentage point by the end of next year.

An increase in rates will impact YOUR monthly mortgage payment. Your housing expense will be more a year from now if a mortgage is necessary to purchase your next home.

3. Either Way You are Paying a Mortgage

As a recent paper from the Joint Center for Housing Studies at Harvard University explains: “Households must consume housing whether they own or rent. Not even accounting for more favorable tax treatment of owning, homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord plus a rate of return. That’s yet another reason owning often does—as Americans intuit—end up making more financial sense than renting.”

4. It’s Time to Move On with Your Life

The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears that both are on the rise. But, what if they weren’t? Would you wait? Look at the actual reason you are buying and decide whether it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer or you just want to have control over renovations, maybe it is time to buy.

Bottom Line

If the right thing for you and your family is to purchase a home this year, buying sooner rather than later could lead to substantial savings.

Monday, September 8, 2014

Tuesday, September 2, 2014

Subscribe to:

Posts (Atom)