If you are thinking about purchasing a home right now, you are surely getting a lot of advice. Though your friends and family have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Let’s look at whether or not now is actually a good time for you to buy a home. There are three questions you should ask before purchasing in today’s market:

If you are thinking about purchasing a home right now, you are surely getting a lot of advice. Though your friends and family have your best interests at heart, they may not be fully aware of your needs and what is currently happening in real estate. Let’s look at whether or not now is actually a good time for you to buy a home. There are three questions you should ask before purchasing in today’s market: 1. Why am I buying a home in the first place?

This truly is the most important question to answer. Forget the finances for a minute. Why did you even begin to consider purchasing a home? For most, the reason has nothing to do with finances. A study by the Joint Center for Housing Studies at Harvard University reveals that the four major reasons people buy a home have nothing to do with money:

- A good place to raise children and for them to get a good education

- A place where you and your family feel safe

- More space for you and your family

- Control of the space

What non-financial benefits will you and your family derive from owning a home? The answer to that question should be the biggest reason you decide to purchase or not.

2. Where are home values headed?

When looking at future housing values, Home Price Expectation Survey provides a fair assessment. Every quarter, Pulsenomics surveys a nationwide panel of over one hundred economists, real estate experts and investment & market strategists about where prices are headed over the next five years. They then average the projections of all 100+ experts into a single number. Here is what the experts projected in the latest survey:

- Home values will appreciate by 4% in 2015.

- The cumulative appreciation will be 19.5% by 2018.

- Even the experts making up the most bearish quartile of the survey still are projecting a cumulative appreciation of over 11.2% by 2018.

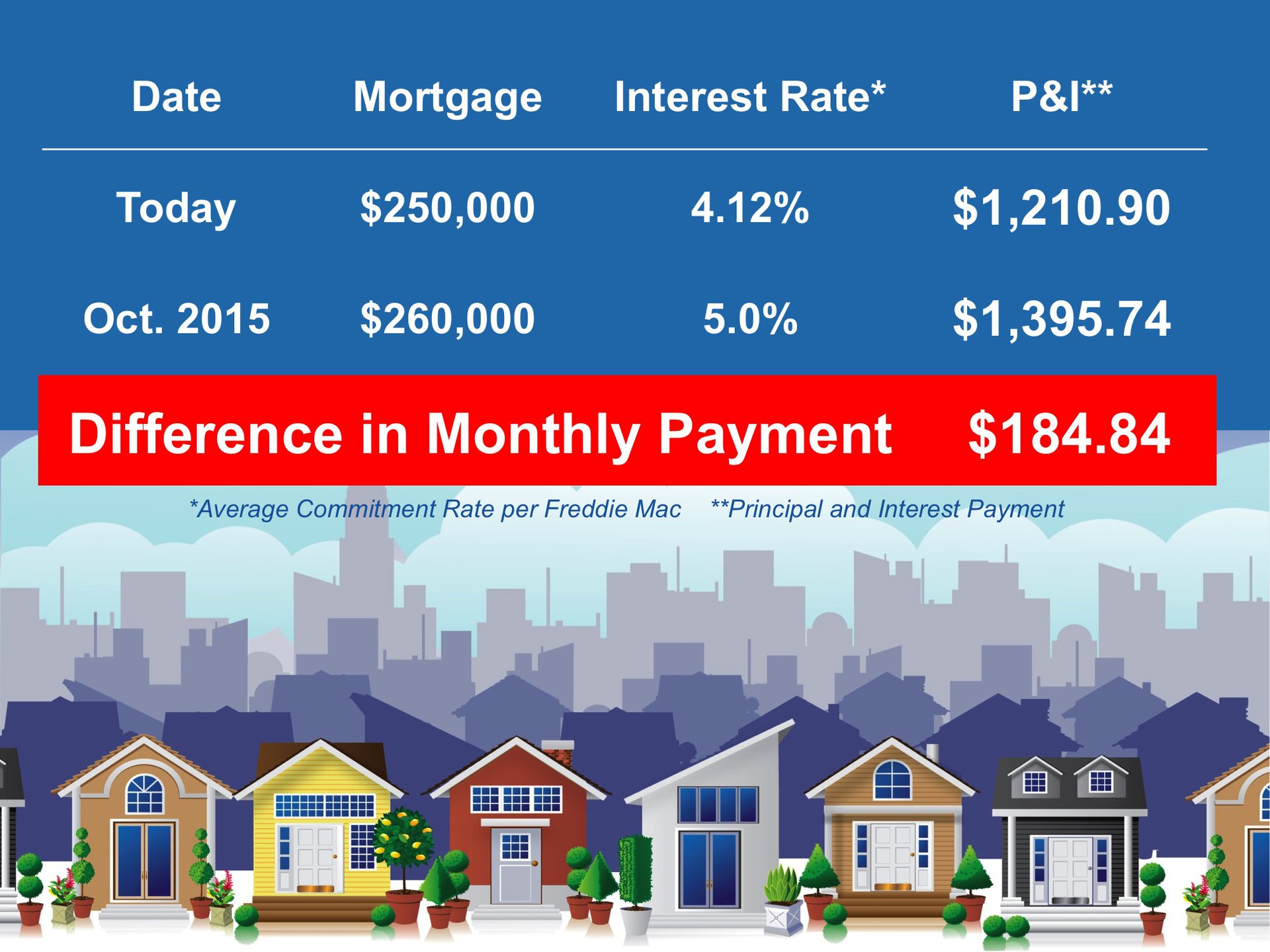

3. Where are mortgage interest rates headed?

A buyer must be concerned about more than just prices. The ‘long term cost’ of a home can be dramatically impacted by an increase in mortgage rates. The Mortgage Bankers Association (MBA), the National Association of Realtors, Fannie Mae and Freddie Mac have all projected that mortgage interest rates will increase by approximately one full percentage over the next twelve months.

Bottom Line

Only you and your family can know for certain the right time to purchase a home. Answering these questions will help you make that decision.

The National Association of Realtors (NAR) released their

The National Association of Realtors (NAR) released their

Billionaire money manager John Paulson was

Billionaire money manager John Paulson was

For the last several years, home sellers had to compete with huge inventories of distressed properties (foreclosures and short sales). The great news is that the supply of these properties is falling like a rock in the vast majority of housing markets (only

For the last several years, home sellers had to compete with huge inventories of distressed properties (foreclosures and short sales). The great news is that the supply of these properties is falling like a rock in the vast majority of housing markets (only  We have often talked about the difference between COST and PRICE. As a seller, you will be most concerned about ‘short term price’ – where home values are headed over the next six months. As either a first time or repeat buyer, you must not be concerned about price but instead about the ‘long term cost’ of the home.

We have often talked about the difference between COST and PRICE. As a seller, you will be most concerned about ‘short term price’ – where home values are headed over the next six months. As either a first time or repeat buyer, you must not be concerned about price but instead about the ‘long term cost’ of the home.

A recent

A recent  Today we are excited to have Nabil Captan as our guest blogger. Nabil is a nationally recognized credit scoring expert, educator, author and producer. In today’s post, he explains how what you don’t know about your credit score could end up costing you. Enjoy! – The KCM Crew Informed consumers considering a home purchase today want to do the right thing and plan ahead. Many do not seek immediate professional guidance from a Realtor or a mortgage loan officer. Instead, they hunt for hours online, looking at numerous websites for available homes for sale. They also consult websites to find the best interest rate and terms for future monthly mortgage payments. Many consumers feel betrayed, cheated and at times embarrassed to learn that the credit scores they counted on, to get that specific interest rate for their loan, are not used by mortgage lenders. When shopping for a good mortgage interest rate, consumers also need to know their credit score, and utilize an online mortgage calculator to compute future monthly mortgage payments. A Google search for “credit score” will yield hundreds of results. The consumer accepts the provider’s terms and conditions to get a free credit score. Terrific! Unaware that in exchange they just received a meaningless credit score that lenders never use. They also handed over their Non-Public Personal Information (NPPI) to that credit score provider for life. Before we go any further, let’s look at available credit scoring products available to consumers today:

Today we are excited to have Nabil Captan as our guest blogger. Nabil is a nationally recognized credit scoring expert, educator, author and producer. In today’s post, he explains how what you don’t know about your credit score could end up costing you. Enjoy! – The KCM Crew Informed consumers considering a home purchase today want to do the right thing and plan ahead. Many do not seek immediate professional guidance from a Realtor or a mortgage loan officer. Instead, they hunt for hours online, looking at numerous websites for available homes for sale. They also consult websites to find the best interest rate and terms for future monthly mortgage payments. Many consumers feel betrayed, cheated and at times embarrassed to learn that the credit scores they counted on, to get that specific interest rate for their loan, are not used by mortgage lenders. When shopping for a good mortgage interest rate, consumers also need to know their credit score, and utilize an online mortgage calculator to compute future monthly mortgage payments. A Google search for “credit score” will yield hundreds of results. The consumer accepts the provider’s terms and conditions to get a free credit score. Terrific! Unaware that in exchange they just received a meaningless credit score that lenders never use. They also handed over their Non-Public Personal Information (NPPI) to that credit score provider for life. Before we go any further, let’s look at available credit scoring products available to consumers today: